The pace of change as the Federal Reserve increases its rate is going to significantly affect Latin American economies. World Finance speaks to Robert Wood from The Economist Intelligence Unit at the Felaban 2015 conference.

Month: November 2015

Felaban 2015: Trade finance will be hindered by Basel III

Bankers are saying they’re hampered by regulatory rules that don’t allow them to do what they do best. World Finance speaks to Citi’s John Ahearn at Felaban 2015.

Felaban 2015: Frank Vogl on money laundering and the terror threat

Anti-corruption expert Frank Vogl was one of the keynote speakers at Felaban 2015. World Finance caught up with him as he left stage to ask if we’re likely to see any anti-corruption action, or just more good intentions.

Felaban 2015: Cuba’s re-emergence still waiting on US action

Fernando Capablanca, Former Chairman of FIBA, the Florida International Bankers Association, discusses Cuba\’s banking industry at the Felaban 2015 conference.

Felaban 2015: Meet us in Miami

Nearly 2,000 banking leaders from 51 countries are gathering in Miami to discuss timely economic, political and regulatory issues confronting the banking industry. World Finance has been providing authoritative, round the clock coverage of the event for the last four years. Come say hello in the Intercontinental Miami Downtown.

Global dividend payouts get a boost in the US

A strong third quarter in the US economy has seen global dividend payouts increase. Increased growth, alongside strong consumer confidence among Americans saw the amount paid out to share holders increase 2.3 percent, a grand total of $297bn, according to a survey by Henderson Global Investors, reports the Financial Times.

Collectively, dividend payouts in North America were up 20 percent on

the year

Collectively, dividend payouts in North America were up 20 percent on the year, reaching a quarterly record of $116.5bn. Between the two major economies of the region – Canada and the US – the latter saw the biggest boost. The US saw payouts rocket up by 23.4 percent to $107.9bn, which constitutes its seventh quarter of double-digit increases.

While US divided growth benefited from a one off $9.8bn special payout from Kraft due to its merger with Heinz, removing this outlier would still allow for strong US growth figures. “The US is far ahead of the curve, propelling dividends forward at breakneck speed,” said Alex Crooke, head of global equity income at Henderson.

All is not well in the world of dividends, however. China has held global dividend payout growth back with a seemingly poor performance. Growth of dividends from emerging markets distinctly lagged behind. China in particular, addled by slowing economic growth, saw disappointing results. According to the report China is “on course for the first ever decline in Chinese dividends.”

The poor figures from China have, according Crooke, “come sooner than we expected. Payouts from Chinese companies have nearly tripled in six years, but a fall in the country’s total payout is likely in 2015 for the first time’’.

Japan in recession fourth time since financial crisis

Japan has again slipped into a technical recession, after preliminary data for the third quarter showed the national economy had contracted for a second consecutive quarter. The relapse is the country’s fourth since the financial crisis, and likely means more stimulus will be needed to arrest the slide and keep inflation closer to the central bank’s two percent target.

The results were not altogether surprising after a 0.7 percent slump hit in the second quarter

“The second straight contraction in GDP underlines the downside risks to the Bank of Japan’s growth forecasts,” wrote Capital Economic’s Japan Economist Marcel Thieliant in a research note. “With rising slack dampening price pressures, we remain convinced that more monetary stimulus will eventually be needed.” In the same note, Thieliant goes on to warn that policymakers have shown “considerable reluctance” to step up the pace of easing, and are unlikely to do so in the coming week.

The results were not altogether surprising after a 0.7 percent slump hit in the second quarter. And though the contraction this last quarter is only 0.2 percent, it means the economy has shrunk 0.8 percent on an annualised basis. Companies, despite record profits, are reluctant to raise wages or invest, and the same findings show that business spending fell 1.3 percent on the quarter last, whereas private consumption rose only 0.5 percent.

Aside from Japan’s less-than-impressive performance, there are positives for the country going forwards. “Firms’ forecasts for industrial production suggest that the economy should start to recover this quarter,” said Thieliant. “But we think that growth in the current fiscal year will be closer to 0.5 percent rather than the 1.2 percent projected by the Bank of Japan at its end-October meeting.”

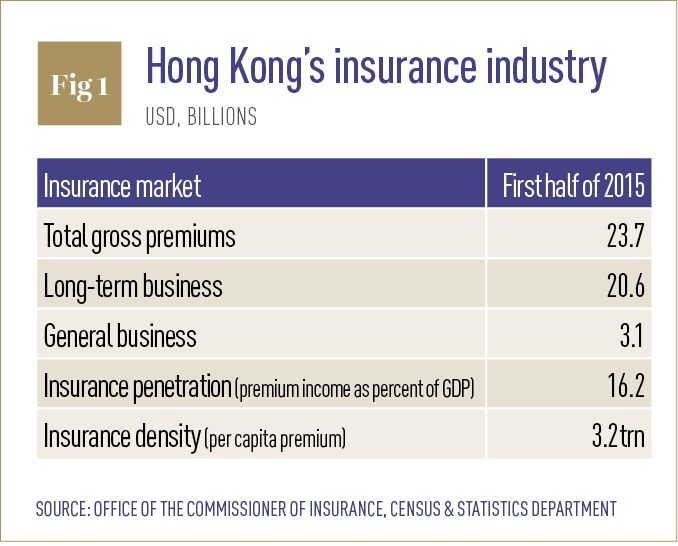

HSBC keeps abreast of developments in Hong Kong’s insurance industry

By keeping a close eye on consumer patterns, HSBC has performed well in Hong Kong’s solid insurance sector (see Fig. 1). The industry’s gross premiums for the first half of 2015 were up 13.6 percent on 2014, and much of the growth was attributed to the long-term insurance business. Endowed with a new regulatory framework, HSBC is taking strides to make good on new opportunities.

With a strong heritage and brand, HSBC is well placed to grow its Hong Kong insurance business as it looks to build on its 150 years of experience by improving its standing both locally and internationally. As a global and universal bank, the group serves customers from over 6,100 offices in 72 countries and territories, meaning that its Hong Kong insurance business can benefit from other key markets for HSBC, sharing their strengths, experiences and findings. Speaking on the group’s purpose, Candy Yuen, CEO of HSBC Insurance Hong Kong, stressed that its operations are united by a singular ambition to connect its customers to opportunities: “we enable businesses to thrive and economies to prosper, helping people fulfil their ambitions”. The bank also enjoys a distinct advantage over its competitors in that it already boasts a strong local presence in the Hong Kong insurance and Mandatory Provident Fund (MPF) market, where it is the leading player in the latter and one of the top players in life insurance business.”

HSBC boasts quite a few advantages when it comes to making good on the opportunities in Hong Kong

A focus on the customer

“Customers have been and will always be at the centre of everything we do”, said Yuen, speaking on the importance of strong customer relationships in realising new insurance opportunities in the market. “We are committed to do the right things for our customers in whatever we do. For example when we develop our insurance products, we start with the customers’ journey, analysing their needs and requirements.”

In terms of face-to-face service, the process is supported by a need-based financial planning process, through which HSBC is able to gauge a good understanding of the financial situation and wealth goals of each individual customer. “At HSBC, we want to really know our customers and therefore we dedicate resources to research and developing surveys to gather insight on what they need. We regularly produce global reports of our findings with our customers such as Future of Retirement and Value of Education”, said Yuen.

HSBC boasts quite a few advantages when it comes to making good on the opportunities at hand in Hong Kong. However, of equal importance is a thorough understanding of the economic climate and the way in which it has shaped the financial habits of individuals. For instance, a low interest rate environment means that customers now tend to seek attractive total yield on the long term. What’s more, “considering fluctuations in the equity market, customers may look for some investment vehicles that provide a stable return and maybe even certain level of guarantee, so insurance products not only provide comprehensive protection, they are also considered good savings options for certain financial goals”, Yuen added.

Finally, the RMB has been gaining popularity for some years now, and many customers in Hong Kong look for RMB as a currency option for their policies. Regardless of recent fluctuations, the currency, in the long run, is one that many customers will keep an eye on. “Knowing our customers’ preferences, we offer RMB options to our products, where suitable”, said Yuen.

In response to the ever-changing situation facing the locals, HSBC has tailored its products and services to its customer’s preferences. HSBC’s Income Goal Insurance Plan is a classic example, and the ‘grow-defend’ insurance solution targets customers looking for upside potential and steady income and caters for their education, wealth accumulation and retirement planning needs.

The HSBC Hong Kong’s Wealth Tracker 2014 report, which takes into consideration 1,000 individuals aged 18-65, indicates that children’s education, retirement expenses and mortgage repayments are currently in the top of minds of customers in Hong Kong. “As people progress through different life stages, their needs and life goals change. People who plan early are more likely to be in a better financial position as they have a longer investment horizon, can take more risk and are able to adjust their strategies”, said Yuen. Based on the insights, HSBC has created insurance solutions that allow customers to save for long term goals, such as education and retirement, while ensuring there’s sufficient protection for unforeseen events.

“Leveraging our strong brand and the strengths of the HSBC Group, Insurance Hong Kong is well positioned for further expansion and growth”, said Yuen. “In tandem with the group’s strategy, HSBC Insurance Hong Kong plays a critical role in the development in Asia, Pearl River Delta [PRD] in particular. HSBC intends to accelerate investments in Asia, developing its business in both the PRD in Guangdong province, China, and in the ASEAN region. HSBC will expand asset management and insurance in Asia with the aim of capturing significant opportunities from emerging wealth in the region. As part of the PRD, we are dedicating resources to accelerate the development of our Hong Kong insurance business.”

Personalised digitisation

The goal for HSBC Hong Kong is to deepen the bank’s relationship with its customers, and in doing so better serve different customer needs. Digitisation is also a major focus for the bank, and HSBC has been enhancing its platforms to create a customer centric, digitally enabled service. Allowing customers to conduct their business and manage the way they have contact with the bank, in a way they choose.

As with any other medium, customer experience is of the utmost importance: “We want to know our customers and their digital behaviour so we can deliver the best service and products to them,” added Yuen. “We have recently enhanced our platform and website. We will continue to improve our digital capabilities and mobile journey to make them simpler and easier for customers to use and navigate.” Yuen continued: “From time to time, we revisit the tools used by our branch staff and capture new technology – for example tablets with special purpose apps, which should serve to save time, paper and generally improve the customer’s in-branch and online experience.”

Knowing that customers appreciate the convenience of buying products online and on mobile, HSBC is constantly looking at new products that could be made available online. Already, the company sells more travel insurance online than it does through any other channel, and making more products and services available online means that customers can set about conducting their affairs in whatever way they want, whenever they want. However, while there are opportunities, there are also challenges for HSBC.

The challenges of regulatory change and the ever competitive landscape warrant attention. According to HSBC Hong Kong, the best answer to these challenges is to simply revert back to the most basic of principles, otherwise defined as the group’s purpose, which consists of connecting customers to opportunities. “We all need to stay focused, take ownership and be at our best for our customers and deliver the best experience we can.”

Looking at Hong Kong’s prevailing trends, HSBC notes that much of the opportunities will lie in health products, protection and wealth management products, with digital playing a key part too, as an ageing population increases demand for filling retirement and protection gaps and technology gives rise to rapid changes in customer behaviour. “As a prudent insurer, we have been monitoring these trends in order to set our short, medium- and long-term plan and make sure we adapt to the changing needs of our customers,” said Yuen.

AYA Bank transforms Myanmar’s banking sector

Myanmar’s banking sector reached a key milestone last year when it decided to open its doors to foreign banks for the first time, consequently summoning the attention of the international banking community. In the months since, Myanmar’s performance within the sector has been extraordinary, yet the lion’s share of growth has been spearheaded not by these new international arrivals, but by experienced local names. In a time when emerging markets are struggling to maintain their explosive growth rates of old, Myanmar, guided by a strong banking sector, remains on the upward curve.

Of the banks that have contributed to the industry’s development so far, none has played a more important part than AYA Bank, which has pushed the envelope of what can be achieved time and time again. U Phyo Aung, Managing Director of AYA Bank, spoke to World Finance about the sector’s evolution over recent months, and the ways in which the bank is paving the way for future developments.

How has banking in Myanmar evolved?

The country’s banking sector has evolved substantially over recent years. However, Myanmar is still regarded as one of the world’s most ‘under-banked’ countries: according to a PwC report, bank loans comprise only 19 percent of GDP, with only about 30 percent of adults claiming to have any kind of access to financial services.

19%

Bank loans’ contribution to total GDP

30%

of adults in Myanmar are currently banking

40%

AYA Bank’s goal for bankable population in 2020

Nevertheless, the government is working to increase the bankable population to 40 percent by 2020, by implementing such positive steps as the passing of the Central Bank of Myanmar Law in July 2013. This law resulted in the formation of an autonomous central bank that is responsible for the nation’s monetary policy as a whole.

In October 2014, nine banking licenses were awarded to foreign banks, allowing them to enter the country’s banking sector for the first time. The entry of these international firms has provided local banks with the incentive to improve their services in order to take full advantage of the new opportunities provided by their presence, including access to cheaper capital, improvement in management and technology, and the development of a regulatory framework.

The central bank has also announced a plan to deepen the financial market, with further plans to establish a capital market and to push towards financial inclusion, which in itself will include the introduction of agency banking and micro-financing.

What role does technology have to play in this development?

Myanmar’s banks had been using legacy systems for several years before four new firms, including AYA Bank, were founded in 2010. With the use of advanced technology, AYA Bank has started implementing several new projects, such as setting up the centralised infrastructure architecture and a core banking system. Effective use of this technology means that AYA Bank has become a flagship institution and the fastest growing bank in Myanmar.

This achievement has caused many other banks to be drawn to the industry, and as a result many of these banks have now begun to implement their own technology-driven digital delivery channels, such as ATMs, internet banking and mobile apps. Effective use of this technology has in turn had a positive effect on the growth and development of the sector.

In what ways does AYA Bank use technology to improve its services and products?

AYA Bank has used advanced technology, such as wireless communications and mobile and web technology, to improve its entire range of products and services. The goal of AYA business in terms of customer interactions is to generate loyalty based on technology-driven digital channels. This initially began with the evolution of technology and the banking community’s subsequent adoption of it: new systems and infrastructure have been designed to take care of the accounts that are related to the bank’s functions and to establish better network connectivity for centralised operations. Advanced web technologies have been used to set up the first ever internet banking services in the industry, together with the first 2FA implementation for user and transaction authentication.

What further technological developments does AYA Bank have planned?

The bank has expanded its mobile financial services in order to offer new products to its customers, including those who are currently un-banked. AYA Bank is also developing new products that will contribute to the efficiency of self-service platforms, in addition to converting all systems on virtualisation, hosting private cloud computing and improving security on a variety of networks.

What benefits does internet banking bring to Myanmar’s banking sector?

Internet banking with AYA Bank offers customers the opportunity to make online transactions in a truly secure manner. Ours was the inaugural service within Myanmar’s banking sector, providing fund transfers, mobile top-ups, bill payments and more.

How does internet banking help AYA Bank to compete with rivals that are both domestic and regional?

AYA’s iBanking service helps to speed up transactions and provide greater all-round convenience, as customers are able to access their account from any internet-enabled device. Moreover, since the introduction of mobile apps and SMS banking, iBanking has been extended to mobile phone users, thereby allowing customers to manage their accounts from their own pockets. This is a huge competitive advantage for the firm when placed alongside our rivals.

How do you see banking in Myanmar changing in the future?

As Myanmar continues on its rapid economic growth trajectory, the banking sector can expect to see more reforms that will allow it to meet the growing demand that has arisen as a result of the country’s economic development. The ASEAN Economic Community (AEC), which is scheduled to come into force by the end of 2015, will greatly liberalise the flow of goods, services, investment and capital across the member countries, allowing for far greater levels of intra-regional trade. With its geographical position at the crossroads of China, India and several other key ASEAN states and its abundance of rich natural resources, Myanmar is well positioned to benefit from the economic developments in the region. As a major source of leverage for the economy, the banking sector is expected to lead this acceleration in economic growth.

Currently, the top five private banks in Myanmar account for around 80 percent of the sector’s products and services. As their slice of the pie continues to expand, the demand for additional capital is expected to drive consolidation and merger opportunities, as regulators look to create and enhance a new regulation framework – including, among other things, a significantly higher minimum capital requirement.

What does the future look like for AYA Bank?

As the only bank in Myanmar to achieve full IFRS compliance, as well as the first to introduce, successfully implement and operate a centralised core banking system along with a fully functional mobile and internet banking system, AYA Bank has been at the forefront of the country’s banking industry for some time. With the advent of a new banking era, the technological advancements made by AYA and its young workforce – where the average age is under 27 – have already fed into the sector’s general growth efforts.

The governance structure at AYA Bank is both top-down and bottom-up: the board of directors includes professionally qualified and highly regarded non-executive independent directors who ensure that the bank stays in line with corporate governance standards. The bank is also moving towards the adoption and rollout of a customer-centric, omni-channel strategy: by transforming its business into a universal banking platform, AYA’s customers will have access to uniform and holistic banking services.

With its strong branch and ATM network and innovative technologies, AYA Bank will increase the cross-selling opportunities of all financial products to its customers, offering more lucrative non-interest services in order to achieve long-term sustainability.

Having always endeavoured to sit at the forefront of banking innovations and industry development, AYA Bank is confident that it is and will remain well poised to tackle future challenges: as Myanmar’s banking sector continues to intertwine more and more closely with the global financial market, the need for a more efficient financial sector and comprehensive risk management policies within the country will only increase.

AYA Bank aspires to be the best in the country. Rather than focusing on size or profitability, the real emphasis is on escalating staff capacity, building and sharing ideas with customers, transforming businesses into plug-and-play platforms in order to accelerate entrepreneurship, and having an overall deeper social impact on the community at large.

All of this, which must be achieved while maintaining corporate governance standards and embracing sustainable progress in the exciting Myanmar banking landscape of tomorrow, firmly distinguishes AYA Bank from its competitors, both within the region and beyond.

Ocidental on Portugal’s return to greatness

Portugal’s economy has shown signs of real progress lately, having overcome a series of obstacles, and in doing so has handed a boost to its insurance sector. The country’s gathering recovery has instilled a heightened awareness in the public about the importance of financial planning, which has brought with it new opportunities, particularly for the life insurance segment.

The life insurance market last year posted its second consecutive year of growth, up 12.9 percent on 2013, due mostly to increased demand for savings and retirement products. Demand for the latter was up 57 percent last year, revealing customers’ appeal for these solutions, as a ‘safe harbour’ for their long-term savings needs in a context of the still unconsolidated recovery of the financial sector.

“It is a mature insurance market, where life insurance premiums represent six percent of GDP, and that in recent past has been submitted to several consolidation movements, involving major players”, Manuel Lupi Bello, an Executive Committee member at Ocidental, one of Portugal’s leading lights in the Portuguese insurance market, told World Finance.

12.9%

Growth in the Portuguese life insurance industry in 2014

Ocidental Vida is a joint venture between Ageas – an international insurance group, ranked among the top 20 in Europe – and Millennium bcp – the largest private bank in Portugal. The group is also the country’s market leader, with €9.7bn ($10.91bn) in mathematical provisions, and has kept a tight hold on this position in each of the last 10 years, boasting a 22.5 percent market share in 2014. The continued solidity of the joint venture is one of the group’s key pillars of success and by utilising this amalgamation of expertise across a wide array of areas Ocidental is seen as one of the region’s leading insurers.

A winning partnership

“It’s a winning partnership. Bancassurance is the highest growing channel in life insurance and our lifetime distributor partner is none other than Millennium bcp, the leading private bank”, said Bello.

“We act by the principle that each customer is unique. Operating in a mature and demanding market, where customer behaviour is increasingly veering towards personalisation, is a constant challenge for both entities. The bank has a deep knowledge of customer profiles and their needs, so it manages to meet these high expectations. At the same time, we are able to incorporate this expertise in our product development, and this flexibility and quality allows us to match our products to often very different customer profiles. By matching and fine-tuning these two realities, we have been able to build one of the most successful bancassurance operations in Europe and even worldwide.”

The market is not without its challenges, and there are a number of issues for firms such as Ocidental to first consider if they’re to make good on the country’s rapidly evolving insurance space. “I would put the emphasis on three different levels”, said Bello. Speaking first on the regulatory landscape, the Solvency II directive will change a great deal for customers and insurers alike. There are also issues to consider with regards to market consolidation and the consequences here for some of the major insurance players’ shareholders structure. Third, there is a growing awareness of the protection needs for retirement, as well as savings reinforcement, which is already visible in the growth of these lines of business.

“As a major challenge I would highlight the capacity to stay agile and innovative in order to provide the appropriate response to customer needs in ever-changing market conditions”, said Bello. “At the same time, trust and credibility are key, for in the long run the winners will be those who most adequately stick to these principles.”

Ocidental’s market leadership is underpinned by a customer-centric approach and supported by a broad portfolio, covering everything from investments, to savings, retirement and risk, which each have to be aligned with market reality and demands. This allows the company to provide the right answers in meeting customer expectations.

The ultimate goal

“Following our four year strategic agenda, entitled Vision 2015, we have successfully balanced our product mix and fully renewed our offer, and have been able to grab growing opportunities and quickly adapt to market conditions”, said Bello. “The ultimate goal is to bring more interesting returns for customers and protect our portfolio profitability at the same time. For instance, in savings we made a decisive shift from long-term guaranteed rates to pre-announced yearly rates, while achieving a 75 percent growth in 2014 and currently (July 2015) we keep growing and outperforming the market. On unit-linked (UL) products, we strengthened the weight of open ULs in our total UL portfolio, up from 21 percent in 2013 to 58 percent in 2014. As such, we benefit from a more balanced business mix, and we’ve achieved a major transformation in a record time.” The company’s open UL inflow evolution has also proved impressive (see Fig. 1).

Speaking on how the company has adapted to the new regulatory landscape, Bello said: “As life-market leaders, and as part of the Ageas Group, we started our preparation for Solvency II back in 2007.” Having achieved excellent Solvency I ratios, Ocidental has been implementing a broad set of initiatives spanning the entirety of the company, “which in due time prepared us for the coming regime”, he continued. “The transformation of our aforementioned life offer is part of it. Since we’ve done our homework properly we have outperformed the market on EIOPA stress tests in 2014 and are fully prepared for Solvency II.”

A key part of the group’s success in forging strong relationships with customers lies in its ability to tailor solutions accordingly, while also securing the best possible return. The basis for this success rests with the pursuit of rigorous and careful asset management, created in order to safely provide the best returns. “Full transparency and adequately managing expectations are crucial”, said Bello. “For example, our investment and retirement products are structured in different risk strategies and expected returns, according to our customers’ needs. We operate in bancassurance, which means we have to find an adequate response to segments, ranging from private banking to mass market with added value. It is a constant challenge.”

One notable example of this diversity in action is Seguro Investidor Global, which is an investment product with five different investment strategies. Each is tooled according to a specific customer profile and the product has delivered impressive returns to customers utilising an assertive asset management strategy. Transparency together with an ability to make good on new market opportunities and a legacy of impressive achievements allows Ocidental to maintain its customers’ trust, which is a key differentiator when it comes to discussing medium to long term products such as retirement.

Strong relationships

Speaking on how Ocidental has been able to forge strong relationships with its customers, Bello said: “It is the outcome of several working years and a daily commitment to customer centricity, which allows us to capture significant volumes in maturities. Customers know we deliver and value our full commitment to providing an excelling service. Our high customer loyalty index is supported by our strong performance, ability to innovate and develop adequate solutions. It’s one of the best indicators of our success.” The integrated bank /insurance model also allows the group to leverage customer loyalty with benefits for all entities involved, whether they be customer, bank or insurer.

In what remains a relatively mature and well-developed insurance market, Ocidental’s agility and efficiency has set it apart from the crowd. Having always invested in streamlining processes and, in doing so, created an agile organisation, the group has made sure that the benefits span the entirety of the value chain. “Our products are subscribed to on the spot and in bank branches in real-time, even in life risk (unless the amount of capital requires medical exams). And even then the process is quick and agile, always accompanied by the point of sale. Another example is that for years our products have been available online, and so too have our servicing features.”

Continuous investment on agility and efficiency goes hand in hand with incorporating the latest innovations, and means that the group can develop products and services distinct from any other in the market. Looking to the future, Ocidental is finalising a new strategic agenda, entitled Vision 2020 and comprising a programme for the next five years. “Two pillars stand out: that we continue to be truthful to our core DNA as a solid and profitable company on which customers can rely; and that we continue to invest on a truly agile organisation which assimilates innovation and takes advantage of our knowledge to engage with and enchant customers”, said Bello. “We aim to serve our customers in the best possible way, in order to renew their trust and be worthy of their recommendation every day.

Kuwait International Bank stays ahead of the game

Kuwait International Bank (KIB) has successfully completed four decades of relentless efforts to become a pioneer of innovation and growth in the banking industry. In 2007, KIB became an exclusive Islamic bank and in just seven years it was recognised as the Best Islamic Bank, Kuwait in both 2014 and 2015 as part of the World Finance Islamic Finance Awards.

We spoke to Sheikh Mohammed Al Jarrah Al Sabah, the Chairman of KIB, about the bank’s new business strategy, what impact pending regulations will have on banking sector and the growing competition in the Islamic finance industry.

KIB is developing an extended strategy for 2015-20. How do you envision the growth of the bank as a result?

The KIB executive management team developed a five-year strategy for 2015-2020 in collaboration with a top-tier global management-consulting firm. The new strategy sets high aspirations for the bank in terms of market growth, customer partnerships and employee propositions. Our aim is to position KIB as the Islamic bank of choice in Kuwait. KIB’s new strategy is customer centric and involves a significant change in service quality and delivery of our banking and advisory services. Together with our clients, we will seek to play a key role in contributing to the economic development of our beloved country.

195%

KIB’s provisions and collaterals ratio, mid-2015

KIB has indeed reached a pivotal crossroad in its history. Prior to the initiation of our new strategy development and implementation venture, we thoroughly restructured our core departments and launched new businesses. In addition, we diversified our revenue sources and strengthened our positioning on core customer segments. Our balance sheet is now stronger than ever and we are proud to announce that KIB is ready to leap to new to its true potential.

We are truly optimistic about our potential to achieve strong results in 2015 and to grow significantly over the next five years. In spite of uncertain economic outlooks in local and regional markets, we have achieved strong results in the first three quarters of 2015 and are confident that the bank will be able to weather any challenges it encounters. This initial testimony of the new face of KIB is a glimpse of what is yet to come. We are very excited to share this journey with our valued employees and customers and look forward to continue on winning plaudits in the Islamic banking industry and beyond.

Have the Islamic banks recovered from the financial crisis once and for all?

Yes, to a great extent. Several factors helped Islamic banks in warding off vulnerability from the global financial crisis such as their modus operandi, the robust regulatory systems in Kuwait and the efficient leadership of the Central Bank in executing effective recovery measures. The best international regulatory practices were also implemented to accelerate the process of recovery.

KIB, thanks to its management, the staff and the various committees for their sincere and concerted efforts, has brought down the alarming proportion of non-performing loans from 21.4 percent in 2014 to 4.42 percent in the first half of 2015 (against 5.6 percent in the first half of 2014). In addition we increased the provisions and collaterals ratio to 195 percent in mid-2015 compared to 192 percent in the previous year.

Does KIB intend to arrange a syndicated loan with other banks or participate in any development projects?

As for syndicated loans, KIB is exploring new opportunities in the market. As for our participation in development projects in the country, particularly in the oil sector, we are seriously pursuing the financing of a number of development projects that conform to bank’s policy, either solely or through alliances with other banks, for instance the desalination plant project, all in full conformity with the provisions of Islamic sharia.

In fact, ever since its inception, KIB has contributed to the economic growth in the state, starting with the construction sector to establishing specialised divisions supporting and financing different economic sectors. This includes participation in contracting projects, commercial activities, financing SMEs (as they are deemed to be the milestones for diversifying the economy), increasing the private sector contribution in economic growth, improving the efficiency of labour market, and encouraging youth innovation.

What impact will Basel III have on KIB’s operations?

We are well aware of the importance of complying with the regulations, which enhance the banking system’s efficiency and ability to actively respond to any present or future financial development – especially in a way that improves the local banks’ capability to manage risks and protect the stakeholders’ rights via enhancing transparency among banking institutions. In this context we have been always keen on applying the central bank’s regulations pertinent to Basel III. KIB’s financial indices, particularly those related to Basel III regulations, show higher figures against the regulatory requirements – KIB’s capital adequacy ratio exceeded 24 percent and the leverage ratio exceeded 11 percent at the end of the first half of 2015.

Are the regulations imposed by the Central Bank of Kuwait necessary?

I have no doubt that they are indeed necessary. The repercussions of the global economic crisis entail a more vivid regulatory role over the financial institutions all over the world. We at KIB have always been keen on complying with all regulations and roles rendered by the central bank and other regulatory bodies in Kuwait as we believe in the importance of these regulations in enhancing the stability of the banking sector. In this context I should praise the pioneering and proactive role of the central bank of Kuwait under the guidance of Governor Dr Mohammad Y Al-Hashel.

In your annual report, you mentioned the bank intends to focus on the retail sector. What are KIB’s plans in this regard?

At KIB we have felt the need to pay special attention to the retail sector as it represents the milestone between the bank and its customer base. So we give special attention at different levels, including but not limited to, the expansion of the branch network, which will total 30 branches by the end of this year.

This is to provide our quality services to all customers throughout all governorates in the state. Naturally, a similar increase in the number of ATMs, increasing POS terminals, improving the quality of e-services, and social media channels, have all been well-defined to achieve our objectives. These factors, we believe, will create more appropriate and modern Islamic financial products on time. We also plan to classify the customers as per their particular needs and preferences so as to reach out and fulfil all our customers’ diverse requirements.

More banks are emerging in the Islamic banking local market – your comments?

KIB expects an increased demand on the Islamic banking services in the coming years, as shown by a number of recent related studies all around the world. However we still believe that the local Islamic banking market is currently saturated and that local Islamic banks are capable of providing sufficient and adequate services to their customers.

Do you think that the growth of Islamic banks will affect conventional banks?

Basically, Islamic and conventional banks vary in their method of operation and their objectives. Both models managed to achieve sustainable levels of returns and growth in the past few years. This, of course, places the banking sector as one of the major pillars of the Kuwait economy. All banks, whether of Islamic or conventional nature, are competing to serve their customers.

Nevertheless, at KIB we hope to have a greater demand for our Islamic banking products and services in the future. We are also aware of the urgency in the Islamic banking industry, which urges us to create such products and services in order to meet our customers’ current and future expectations.

What are the challenges facing the Islamic banking industry in Kuwait and the region as a whole?

Under the present circumstances, the Islamic banking sector faces several challenges. First of all, it has to introduce new financial products and services. Next, their legitimacy as per the Islamic sharia should be ascertained and they should be able to attract more clients.

Allowing conventional banks to diversify their business model to include sharia-compliant services is also deemed to be another challenge to Islamic banks. A further challenge is the ever-changing regulatory requirements, a prompt response to global and local economic developments.

The increase in banking institutions has resulted in sharp competition against limited investment opportunities and there is a notable absence of catalysts that will accelerate the growth of private sector’s contribution to the local economy, which requires an ongoing process of enhancement to the institutions’ products and services suite.

In spite of the impending challenges encountering the Islamic banking industry, we, with our optimistic outlook, work hard on experimenting, analysing and scrutinising the core issues to overcome these challenges and enhance our capability to compete in the local market so as to continuously provide distinguished services to our customers

Helping poor countries could be crushing them in the long-run

In Scotland, I was brought up to think of policemen as allies and to ask one for help when I needed it. Imagine my surprise when, as a 19-year-old on my first visit to the US, I was met by a stream of obscenities from a New York City cop who was directing traffic in Times Square after I asked him for directions to the nearest post office. In my subsequent confusion, I inserted my employer’s urgent documents into a trash bin that, to me, looked a lot like a mailbox.

Europeans tend to feel more positively about their governments than do Americans, for whom the failures and unpopularity of their federal, state, and local politicians are a commonplace. Yet Americans’ various governments collect taxes and, in return, provide services without which they could not easily live their lives.

Americans, like many citizens of rich countries, take for granted the legal and regulatory system, the public schools, healthcare and social security for the elderly, roads, defence and diplomacy, and heavy investments by the state in research, particularly in medicine. Certainly, not all of these services are as good as they might be, nor held in equal regard by everyone; but people mostly pay their taxes, and if the way that money is spent offends some, a lively public debate ensues, and regular elections allow people to change priorities.

Without effective states working with active and involved citizens, there is little chance for the growth that is needed to abolish global poverty

All of this is so obvious that it hardly needs saying – at least for those who live in rich countries with effective governments. But most of the world’s population does not.

State control

In much of Africa and Asia, states lack the capacity to raise taxes or deliver services. The contract between government and governed – imperfect in rich countries – is often altogether absent in poor countries. The New York cop was little more than impolite (and busy providing a service); in much of the world, police prey on the people they are supposed to protect, shaking them down for money or persecuting them on behalf of powerful patrons.

Even in a middle-income country like India, public schools and public clinics face mass (unpunished) absenteeism. Private doctors give people what (they think) they want – injections, intravenous drips, and antibiotics – but the state does not regulate them, and many practitioners are entirely unqualified.

Throughout the developing world, children die because they are born in the wrong place – not of exotic, incurable diseases, but of the commonplace childhood illnesses that we have known how to treat for almost a century. Without a state that is capable of delivering routine maternal and child health care, these children will continue to die.

Likewise, without government capacity, regulation and enforcement do not work properly, so businesses find it difficult to operate. Without properly functioning civil courts, there is no guarantee that innovative entrepreneurs can claim the rewards of their ideas.

The absence of state capacity – that is, of the services and protections that people in rich countries take for granted – is one of the major causes of poverty and deprivation around the world. Without effective states working with active and involved citizens, there is little chance for the growth that is needed to abolish global poverty.

Foreign aid

Unfortunately, the world’s rich countries currently are making things worse. Foreign aid – transfers from rich countries to poor countries – has much to its credit, particularly in terms of health care, with many people alive today who would otherwise be dead. But foreign aid also undermines the development of local state capacity.

This is most obvious in countries – mostly in Africa – where the government receives aid directly and aid flows are large relative to fiscal expenditure (often more than half the total). Such governments need no contract with their citizens, no parliament, and no tax-collection system. If they are accountable to anyone, it is to the donors; but even this fails in practice, because the donors, under pressure from their own citizens (who rightly want to help the poor), need to disburse money just as much as poor-country governments need to receive it, if not more so.

What about bypassing governments and giving aid directly to the poor? Certainly, the immediate effects are likely to be better, especially in countries where little government-to-government aid actually reaches the poor. And it would take an astonishingly small sum of money – about 15 US cents a day from each adult in the rich world – to bring everyone up to at least the destitution line of a dollar a day.

Yet this is no solution. Poor people need government to lead better lives; taking government out of the loop might improve things in the short run, but it would leave unsolved the underlying problem. Poor countries cannot forever have their health services run from abroad. Aid undermines what poor people need most: an effective government that works with them for today and tomorrow.

One thing that we can do is to agitate for our own governments to stop doing those things that make it harder for poor countries to stop being poor. Reducing aid is one, but so is limiting the arms trade, improving rich-country trade and subsidy policies, providing technical advice that is not tied to aid, and developing better drugs for diseases that do not affect rich people. We cannot help the poor by making their already-weak governments even weaker.

Angus Deaton is the 2015 Nobel Laureate in economics

© Project Syndicate 2015

The BRICS fallacy

The recent downgrade of Brazil’s credit rating to junk status was followed by a raft of articles heralding the crumbling of the BRICS (Brazil, Russia, India, China, and South Africa). How predictable: schadenfreude almost always follows bad news about the BRICS, whose members were once hailed as the world’s up-and-coming economic powerhouses and next major political force.

There is something deeper going on here. The world’s seeming obsession with the BRICS’ perceived rise and fall reflects a desire to identify the country or group of countries that would take over from the US as global leader. But, in searching for the ‘next big thing’, the world ignores the fact that the US remains the only power capable of providing global leadership and ensuring some semblance of international order.

Clearly, the BRICS are a thing. They are just not the thing

The story of the BRICS is a familiar one. It began as a technical grouping in 2001, when the British economist Jim O’Neill lumped them together (without South Africa) and gave them their catchy name for the sole reason that they were all large, rapidly growing emerging economies. But, recognising that economic power could translate into political influence, the BRICS held their first informal meeting in 2006, and their first leaders’ summit in 2009. The bloc was going places – or so it seemed. But seven years, seven summits, and one new member (South Africa joined in 2010) later, the significance of the BRICS remains hotly debated.

Cracks in the foundations

The disparities among the BRICS are well known. China’s economic output is nearly twice that of the rest of the BRICS combined, and roughly 30 times that of South Africa. Their governance models are vastly different, from India’s robust democracy to Russia’s illiberal model to China’s one-party system. Russia and China, both permanent members of the UN Security Council, have offered, at best, lukewarm support for the other BRICS’ aspirations to join them. And then there are its members’ bilateral disagreements, including a heated territorial dispute between India and China.

Nonetheless, the BRICS have acted in concert on more than one occasion. Last March, amid near-universal condemnation of Russia’s annexation of Crimea, the country’s BRICS counterparts – even those that had long supported the inviolability of borders and non-intervention – abstained from a UN General Assembly resolution affirming Ukraine’s unity and territorial integrity.

Three months later, the BRICS released their Leaders’ Summit Declaration condemning the imposition of economic sanctions on Russia by the EU and the US. Most concretely, the long-anticipated New Development Bank, run jointly and equally by the five BRICS countries, opened its doors in Shanghai in July. Clearly, the BRICS are a thing. They are just not the thing.

The BRICS arose at a time when much of the world, especially the advanced economies, was mired in crisis. The ‘fall of the West’ narrative ran alongside that of the ‘rise of the rest’. But the story has not played out quite as anticipated.

Economically, the BRICS are facing serious challenges. In addition to a well-documented growth slowdown, China has lately experienced considerable stock-market turmoil and currency devaluation. The Brazilian and Russian economies are contracting; South Africa’s growth has slowed; and India, though maintaining relatively strong growth, must undertake important reforms.

The BRICS have also failed to fulfil their promise of international leadership. At the beginning of the decade, Brazil showed a certain aspiration, along with Turkey, to press ahead with an alternative nuclear deal with Iran. But that proposal fell apart, and, amid pressure from corruption scandals and falling commodity prices, Brazil left the global stage.

South Africa and India also continue to punch below their apparent weight internationally (notwithstanding Indian Prime Minister Narendra Modi’s visibility). As for Russia, the only traditional world leader of the bunch, the Kremlin’s Ukraine policy has done severe damage to the country’s international profile – damage not even its possible diplomatic coup in Syria can undo.

Bricks don’t float

Only China has displayed an inclination to lead, as exemplified by President Xi Jinping’s visit to Washington DC last week, which produced major announcements on climate action, cyber security, and international development. China has also been pursuing initiatives like the Asian Infrastructure Investment Bank and the revitalisation of the Shanghai Cooperation Organisation. But China’s growing assertiveness, particularly in the South China Sea, has fuelled the perception that it is more of a threat than a leader. All in all, the BRICS no longer seem to be rising.

At the same time, the core of the West no longer seems to be declining. Although Europe remains mired in crisis and existential self-doubt, and Japan is still finding its feet after two decades of economic stagnation, the US is as relevant as ever. Indeed, no major global challenge – from conflict in the Middle East to climate change to global financial regulation – can be confronted without American engagement. America’s enduring dominance will rile many, and with good reason.

A quarter-century after the Cold War’s end, the world should have arrived at a more equitable and balanced way of getting things done. But it has not, and no other single power is in a position to take America’s place. Europe is too inward looking; China inspires too much suspicion; and India, despite showing signs that it is preparing for a greater global role, lacks enough international authority on its own. As a result, nearly 20 years after former US Secretary of State Madeleine Albright dubbed her country “indispensable”, it remains so.

The imperative now is for the US and the world to recognise this. Rather than focusing our attention on alternatives to US leadership, we should be emphasising its importance – an approach that would help to spur the US to rededicate itself to its international responsibilities. There have been hints that this impulse still exists – notably, the Iranian nuclear deal – but they remain inadequate to the challenges confronting the world.

The international order is at a crossroads. It needs the US to guide it – with ingenuity, initiative, and stamina – in the direction of peace and prosperity. Obsessing about who might eventually replace America is bound to get us all lost.

Ana Palacio is former Senior Vice President of the World Bank and member of the Spanish Council of State

© Project Syndicate 2015

The people’s car decadence

So far, the Volkswagen scandal has played out according to a well-worn script. Revelations of disgraceful corporate behaviour emerge (in this case, the German automaker’s programming of 11 million diesel vehicles to turn on their engines’ pollution-control systems only when undergoing emissions testing). Executives apologise. Some lose their jobs. Their successors promise to change the corporate culture. Governments prepare to levy enormous fines. Life goes on.

This scenario has become a familiar one, particularly since the 2008 financial crisis. Banks and other financial institutions have enacted it repeatedly, even as successive scandals continued to erode confidence in the entire industry. Those cases, together with Volkswagen’s ‘clean diesel’ scam, should give us cause to rethink our approach to corporate malfeasance.

Empty promises

Promises of better behaviour are clearly not enough, as the seemingly endless number of scandals in the financial industry has shown. As soon as regulators had dealt with one case of market manipulation, another emerged.

The trouble with the banking industry is that it is built on a principle that creates incentives for bad behaviour. Banks know more about market conditions (and the likelihood of their loans being repaid) than their depositors do. This secrecy lies at the heart of financial activity. Polite analysts call it ‘management of information’. Critics consider it a form of insider dealing.

11m

Vehicles affected worldwide

40x

The legal limit of nitrogen oxide

$18bn

Potential fines

$7.3bn

Set aside by VW to cover costs of scandal

Banks are also uniquely vulnerable to scandal because many of their employees are simultaneously behaving in ways that could influence the reputation, and even the balance sheet, of the entire firm. In the 1990s, a single Singapore-based trader brought down the venerable Barings Bank. In 2004, Citigroup’s Japanese private bank was shut down after a trader rigged the government bond market. At JPMorgan Chase, a single trader – known as ‘the London Whale’ – cost the company $6.2bn.

What these repeated scandals show is that apologies are little more than words, and that talk about changing the corporate culture is usually meaningless. As long as the incentives remain the same, so will the culture. The Volkswagen case is a useful reminder that corporate wrongdoing is not confined to the banking industry, and that merely levying fines or ramping up regulation is unlikely to solve the problem. Indeed, it is one of the iron laws of corporate physics: for every regulation, there is a proportionate proliferation of innovations to circumvent it.

Rigged results

It should come as no surprise that there were incentives in the automobile industry to game the system. Everyone knows that actual fuel economy does not correspond to the numbers on the showroom sticker, which are generated by tests carried out with the wind blowing from behind or on a particularly smooth road surface. Similarly, anyone who has stood next to a diesel vehicle, even one proclaiming the virtues of ‘clean diesel’, could tell that it was smellier than cars powered by gasoline.

There are two important similarities between the scandals in the finance industry and at Volkswagen. The first is that large corporations, whether banks or manufacturers, are deeply embedded in national politics, with elected officials dependent on such firms for job creation and tax revenues. Volkswagen in particular is an icon of German manufacturing. Chancellor Angela Merkel has gone out of her way to support the company, as did her predecessor, Gerhard Schröder, who came to its defence in 2003, when the European Commission challenged the legality of its holding structure.

The second similarity is that both industries are subject to multiple regulatory objectives. Regulators may want banks to be safer, but they also want them to lend more to the real economy, which often means taking more risks. As a consequence, they impose rules that do not clearly push banks in one direction or the other.

The regulation of automobile emissions faces a similar problem. As regulators’ focus turned toward limiting global warming, there were tremendous incentives to manufacture vehicles that produced fewer greenhouse-gas emissions, even if that meant, as with diesel engines, emitting other gases and micro-particles that are much more harmful to humans in their vicinity.

There was never a discussion of the trade-off between limiting local pollution and fighting climate change. As the Volkswagen crisis so vividly illustrates, we need more than corporate apology and regulatory wrist slapping.

It is time for a sustained discussion about how to craft regulations that provide the proper incentives to achieve the objectives we truly desire: economic and social wellbeing. It is only when that discussion takes place that we will get the banks, cars, and other goods and services that we want.

Harold James is an Economic Historian

© Project Syndicate 2015

Australia’s revolving door of politicians is an embarrassment

Australia has a new prime minister – its fifth in just eight years. No Australian prime minister has served a full electoral term since 2007, and we have had four incumbents in the last 27 months alone. In June 2013, Labor Prime Minister Julia Gillard was defeated in a party-room vote by Kevin Rudd, who lost the post in the general election later that year to the conservative coalition’s Tony Abbott, who has now in turn been defeated in a party-room coup by Malcolm Turnbull.

This latest turn in our prime ministerial carousel has left Australians trying, yet again, to explain to bemused colleagues around the world how this stable bastion of Western democracy, and the world’s 12th-largest economy, could be engaged in such a pantomime. Is it something in the water that makes us want to treat our political leaders like disposable tissues?

There seem to be three different dimensions to the explanation. One is simply the local impact of the impatience that is becoming increasingly obvious in the world’s established democracies. The endless 24/7 media cycle and omnipresent social media are generating a taste for celebrity and an almost pathological preoccupation with current opinion polls, rather than serious political debate. Traditional parties and processes are finding it harder and harder to satisfy the demand for instant gratification.

Is it something in the water that makes us want to treat our political leaders like disposable tissues?

A second dimension is Australia-specific: the tension created by peculiarities of the country’s political system. A ludicrous three-year electoral cycle, shorter than almost anywhere else in the world, makes it almost impossible to govern in a campaign-free atmosphere. And party rules have allowed for leaders – including serving prime ministers – to be torn down overnight by their parliamentary colleagues (although this has now changed for Labor).

The remaining part of the explanation is undoubtedly local and personal: the character quirks that have contributed to each leader’s dramatic rise and equally spectacular fall.

Character quirks

Gillard proved herself to be a highly competent transactional politician: ruthless in grabbing the ascendancy when Rudd seemed to be faltering in the polls; highly effective in negotiating with cross-benchers to keep her minority government alive; and successful in gaining huge local and international attention for her passionate parliamentary assault on her opponents’ perceived misogyny. But on almost every major policy issue, she was tone-deaf in sensing the popular mood, and seemed to have no guiding principles attractive to either her party or the wider public.

Rudd, who wrestled the leadership back from her, is intellectually brilliant and, when on his game, a great campaigner who succeeded in minimising the scale of Labor’s loss in the 2013 election. But the wide respect he garnered internationally for his role in crafting the G-20 response to the global financial crisis did not help with his local colleagues, who saw him as too often incommunicative, obsessive, and lacking judgment in setting policy priorities.

The now-deposed Abbott, a muscular Christian alpha male with profoundly conservative social values, won the leadership of the Liberal Party, and the anti-Labor coalition, as the unexpected beneficiary of a three-way party split in 2009. But while Abbott was a spectacularly effective opposition leader as the Labor government unravelled, he proved himself utterly unable to manage his transition to prime minister, and was trailing badly in the opinion polls when he was ousted.

Abbott presided with slogans, rather than coherent policy, over a rapidly deteriorating economy. He was hyper-partisan, ran against public sentiment on issues like gay marriage and restoring knighthoods, and constantly alienated his ministerial colleagues with solo “captain’s picks” in support of unpopular people and policies.

He’s behind you

Abbott’s nemesis, Turnbull, now Prime Minister, stands in sharp contrast: sophisticated, highly successful in his past lives as a journalist, lawyer, and investment banker, and very popular – across party lines – with the electorate. He is a superbly articulate communicator, a past leader of the anti-monarchist republican movement, and as liberal in his political instincts as Abbott was conservative.

Nonetheless, he was a flop in his brief earlier incarnation as opposition leader in 2008-2009, widely seen as arrogant, non-consultative, and prone to spectacular errors of judgment. But Labor’s hopes that Turnbull will fail to learn from his earlier mistakes – and that the prime ministerial door will continue to revolve – seem likely to be disappointed, at least in the short term.

Turnbull knows that the great majority of his governing coalition does not share his liberal instincts, and that he will have to tread cautiously and collegially on policy change. But he is also smart and articulate enough to know that if he maintains self-discipline, and argues rather than asserts his case, he can change the paradigms.

A new hope

The hope for Australia is that this is a watershed moment, with both government and opposition realising that dumbed-down sloganeering and races to the populist bottom may win short-term advantage, but are ultimately counterproductive. What most voters want is political leaders who have a coherent guiding philosophy, a persuasive policy narrative, and a genuine commitment to a decent governing process.

For all its apparent attachment to superficial policymaking and tabloid personality politics, it is becoming evident that the Australian public is fed up with the political circus of recent years, and wants adults back in charge of the major parties. With Turnbull, and Labor’s Bill Shorten, we seem at last to have leaders right for the long haul. We will have to see whether that hope is realised, but the signs are encouraging. And a lot of other democrats around the world will be hoping that we pull it off.

Gareth Evans is Chancellor of The Australian National University & former Labor cabinet minister

© Project Syndicate 2015