In recent years, the Saudi Arabian economy has begun a period of transformation. Both the government and the private sector are realigning their sights on untapped markets and industries as part of an effort to diversify the country’s oil-based economy. The result has been a fast-paced development of the state’s infrastructure and the creation of new opportunities for corporations of all shapes and size. In turn, this economic shift has had a drastic impact on the Saudi banking industry, which is in a state of expansion.

As such, banking in the country continues to go from strength to strength, being driven forward by growing confidence and recent innovations in technology. Moreover, the Saudi Government is firmly committed to driving the financial industry forward through the implementation of a new regulatory framework and support.

Even with the strides already taken in Saudi banking, there is still a great deal of the market that has not yet been reached. This is especially true because Saudi banks are still underbranched at present, particularly in the country’s most remote areas. Leading the trend in offering an expanding network and meeting evolving customer demands is Saudi Hollandi Bank (SHB), the longest-established provider of financial products in Saudi Arabia. With a focus encompassing the entire spectrum, from big organisations to individuals, SHB is at the forefront of understanding customers and providing adept solutions. World Finance spoke with the company’s CEO, Dr Bernd van Linder, about the expansion of Saudi Arabia’s financial industry and how the bank is preparing for a new economic era in the Kingdom.

Saudi Hollandi Bank

1926

Founded

1,637

Employees

56

Branches

SAR 1.82bn

Net income

SAR 65.15bn

Loans and advances

SAR 96.62bn

Total assets

Notes: Figures from year ending 2014

Tell us briefly about the recent growth of the Saudi Arabian banking industry

The Saudi Arabian economy reported 3.59 percent growth in the first quarter of this year. Combined with strong producer and consumer confidence, this growth underpins a resilient and expanding banking sector. The government’s investment in infrastructure projects and its strategy of diversifying the Kingdom’s oil-based economy is creating more opportunities for private and public sector companies as well as for individuals and their families. The Saudi banks have an important role to play here, supporting large project financing, large, small- and medium-sized enterprises (SMEs), and the growing wealth of the Kingdom’s population.

We are seeing particular growth in areas where the government is focusing its energy in supporting smaller businesses and entrepreneurs, such as SMEs, and in the encouragement of home ownership by individuals. Working in partnership with the government to provide banking services to small companies, while offering additional finance to Saudi families on top of government provided housing loans, means that the banking sector is broadening its services and deepening its impact.

How significant is personal banking for the industry’s ongoing development?

When you consider that the Kingdom is still underbranched compared to other countries, particularly in remote areas away from the major cities, the opportunity is very significant. Because of this, banks have expended their physical presence. For our part, we have grown our branch network by 20 percent over the last year and almost doubled our ATM network over the last two years. We expect this type of growth to be common across the industry in the coming years.

However, it is not just about physical presence in the retail market. The key will be to successfully integrate branch services seamlessly with other channels. Customers should expect to be able to initiate a transaction using one channel and finish it on another, without having to restart or duplicate their activities. Of course, branches will continue to play an important role in the future, but as one part of the overall customer experience rather than as the sole or even the main point of interaction.

All of this is being driven by customer demand and a growing sophistication in customer expectations, encouraged and enabled by technology. As a whole, the industry has seen significant growth in retail banking over the last year and we expect to see that trend continue.

What are the major opportunities and challenges in this area?

Clearly, with the government’s commitment to continue to invest in the economy and its support for private enterprise and families alike, we expect there to be opportunities across the whole spectrum of corporate and retail client segments. Although growth is likely to be strong in all segments, we expect it to be particularly material in the segment of SMEs. We also see an opportunity to help customers in this sector from the perspective of advice, as well as finance. Many entrepreneurs are growing their businesses fast without any previous experience so we are providing structured advisory assistance to them in addition to providing the full range of banking services.

But there are challenges. Competitive pressures are always present and margins are tightening, and we see this intensifying as every bank is recognising the potential of this market. And as technology evolves and customer expectations become more defined and sophisticated, there will be pressure on the banking industry to address these issues quickly and design new services and channels efficiently and securely.

How is SHB preparing for future changes?

We are already known as a force in corporate banking, and we will continue to expand our business with large corporates, but mindful of the trends I mentioned earlier, we have also made significant investment in our support for SMEs and individuals.

We are growing our presence in both of these areas and are proud to have already been recognised for our work through a number of awards. By focusing on providing the solutions we know these customers need to grow their own businesses or manage their personal financial assets, we aim to become the bank the Kingdom always chooses.

What is it that differentiates SHB from others in the industry?

Founded in 1926, SHB was the first bank to operate in the Kingdom and acted as the de facto central bank for some time. So a major differentiator for us is the length of our involvement supporting the Kingdom, its companies, individuals and communities. This brings with it deep knowledge and understanding of the fundamentals that drive every customer segment. We know our customers; we know their requirements, and we are able to provide solutions to meet those requirements. Our customers in turn know that Saudi Hollandi is a bank that will stand by them through economic cycles.

But we don’t rest on our laurels. We know that customers want to access the products and services they need quickly, easily and securely. So we listen to them and create ways to deepen our relationships using a mix of the latest technology, specialised customer service and streamlined processes. From extensive internet banking and our smartphone app, to more ATM services and business banking centres, our corporate, institutional, SME and individual customers can connect to us in even more convenient ways.

This is helping to build real customer loyalty and we are always looking for ways to deepen and reward this. To make our retail offerings more attractive, for example, we have a unique bank-wide rewards programme, which gives customers value at each touch point, earning points when they apply for any product or use an alternative delivery channel, such as internet banking or our mobile app. We want to give our customers something back to thank them for their usage of our products and channels.

Customer deposits, sar billions

2010

41.60

2011

44.68

2012

53.19

2013

61.87

2014

76.81

How does the country’s banking industry compare with other nations in the region?

The sheer scale of the Saudi economy, and the country itself, marks it out from its near neighbours and so poses many more opportunities for growth as well as different challenges in terms of physical reach and service provision. The government has worked hard to establish an effective and robust regulatory regime and today the two main bodies – Saudi Arabian Monetary Agency (SAMA) and the Capital Market Authority (CMA) – are recognised internationally for their strong guidance and support. In fact, today the Kingdom’s banks and financial institutions are at the leading edge of compliance with global banking standards.

This has ensured that the sector has grown steadily and carefully; an approach that is being reflected in the opening of local financial markets to international investors. An exciting development for local institutions and their stakeholders.

Broadly speaking, the Kingdom is relatively underbranched, when compared to similar markets in the region or outside. But we, like others, are addressing this, as I mentioned earlier. Otherwise, the challenges that banks face around the world, not just here in the Gulf, are common to all. Competition, quality of service, channel expansion; just a few of the challenges that banks and their customers worry about.

What role has technology played in the industry’s development?

Since the earliest days of electronic payments and transfers, technological advancements have driven changes in the banking industry at a rapid pace and the banks that have adapted to these quickly have been able to maintain the loyalty of their customers. That trend is still true today. We are now in an age where formal and informal information flows are instantaneous and customers expect to be able to react using the channels they find most convenient. From simple deposit placing, to bill payment, to asset management, our customers expect to be able to transact online and via apps as well as in our branches. So we make continual investments in our current platforms as well as in the work we do to build the channels of the future.

Technology has noticeably transformed the retail banking market and it is a key success factor in preparing and launching any new product for our customers. Used well, and of course marketed and explained well, technology can make banking straightforward and easy and it is a cornerstone of our connectivity to customers of every size and ambition. Consequently, its latest applications are at the core of the training programmes we run for our bankers and their teams.

Can you expand on the importance of multi-channel solutions in the banking industry?

Even though we believe that physical branches continue to play an important role in customer interaction, primarily at the time of customer acquisition, and we expect the number of bank branches in the Kingdom to continue to grow over the coming years, the key will be to have these branches integrate seamlessly with other channels.

Customers want options, so we have to provide them. It is as simple as that. And today technology allows us to develop channels to allow them to access their bank in ever more easy ways.

What examples can you give where technology has helped grow your business?

A great example is our new bank-wide rewards programme. Customers accrue points through their usage of our products and services and use technology for online redemption of these points with vouchers from partner organisations. This also allows us to monitor customer behaviours and trends, which is useful feedback for future tailoring of our services.

Also, recently we launched a completely revamped internet banking system for our corporate customers, which offers many new administration, transaction and global trade services. And we similarly made advances in personal banking to simplify transaction flows and further widen services such as e-statements for loans and mortgages and for registration with credit cards.

One very popular service has been our mobile banking app, which enables customers to perform their essential daily banking transactions on the go. This has already attracted nearly 20 percent of our customers and we expect that percentage to continue to grow during the year. We are also working on the next generation of our mobile app with different designs for smartphones and tablets that include a number of exciting innovations.

How significant has the opening of the stock market to foreign investors been for the banking industry and the economy?

This move has been much anticipated both in the Kingdom and abroad and comes at a time of a strong economy and a growing financial sector. The opportunity is clear – the Saudi stock market capitalisation is larger than all the other GCC stock markets combined and is likely to prove an attractive option for investors wishing to gain direct access to the Kingdom’s growth story. For example, the local insurance market is the second-fastest growing in the GCC and has good potential for further gains due to its low penetration levels, according to Moody’s Investors Service.

The opening of the Saudi market will widen the foreign investor base, which is currently less than one percent of total holdings. Given the size and depth of the market, it is expected that the Kingdom will be included in the main emerging markets benchmark indices in the future, attracting further interest.

This exciting development is being handled with care and caution by the well-regarded regulators and very clear rules have been put in place to ensure that investors with longer-term interest are prevalent.

3.59%

Growth of the Saudi Arabian economy, Q1 2015

What are some of the current opportunities for foreign investors in Saudi Arabia?

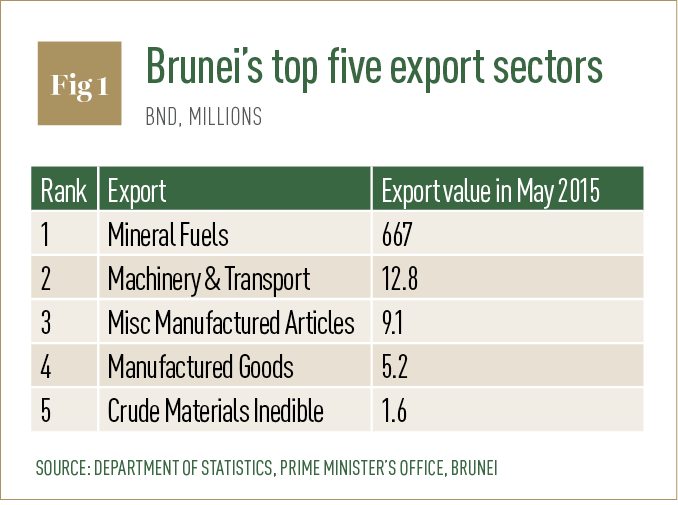

Encouraged by robust GDP growth and macroeconomic stability, both producer and consumer confidence are well above the regional average. Growing private credit and increased public expenditures (see Fig. 1) on infrastructure and other projects provide a broad basis for robust opportunities in Saudi Arabia, and these are translating into particularly strong and sustained growth in domestic demand.

The Kingdom itself has never been more committed to supporting economic growth. As wealth reaches previously less developed areas of the country, attractive opportunities are emerging to cater to pent-up demands in sectors such as healthcare, power and water, and consumer goods.

As the region’s largest economy (see Fig. 2) and the world’s 19th largest exporter, the sheer size of the markets that Saudi-based companies serve is a competitive advantage, allowing Saudi businesses to benefit from economies of scale. With excellent access to Saudi and other MENA markets, as well as the advanced and emerging economies of nearby Europe and Asia, market exposure for Saudi-based companies is not only vast but also highly diversified.

How important has regulation been in facilitating this growth?

The regulators have played a key role in ensuring that the Kingdom’s growth is controlled and well-managed. This applies, for example, to the way in which banks provide the services the Kingdom needs and the very high levels of capital strength with which they are expected to comply.

How would you say Saudi Arabia’s corporate governance standards stack up against those in neighbouring nations?

In Saudi Arabia, corporate governance standards are already high and effort is now being applied to intensify compliance with the opening of the markets to foreign investment. The CMA is continually focused on ensuring compliance, strengthened controls and improved transparency. As a result, listed corporates and banks are exercising great diligence in managing their affairs.

According to the Hawkamah Institute for Corporate Governance, its ESG index, which measures the environmental, social and governance attributes of publicly traded companies in the MENA region, has shown good results for Saudi Arabia. Another attractive trait for international investors.

What are SHB’s ambitions for the future?

We aim to be the bank the Kingdom always chooses and will continue to work hard to that end. There are three key drivers of our approach: efficiency and capital strength, investment in our core businesses and a single-minded focus on our customers. Together with the strong internal culture that helps customers realise every opportunity, these cornerstones will ensure that we continue to grow and to broaden our market presence.