OctaFX is a global broker that has been providing online trading services worldwide since 2011. Looking back on 2021, OctaFX, its departments, as well as its growing community, have much to be proud of and look forward to. Our company maintained its focus on helping clients to achieve their investment goals by providing its services and tools even during the tightest pandemic restrictions.

As a result, the fintech company added many accolades to its name, such as receiving international recognition as the ‘Best Forex Broker, India’ – awarded by World Finance. This reflects 12 months during which the company considerably improved OctaFX’s product, refining it for its clients, bringing a closer, more personable relationship, and making the product experience even more accessible and inspiring for new customers.

The product

The trading mechanics became even more convenient and relevant to our customers’ needs. The launch of the OctaFX trading app for Apple iOS certainly resonated with the trader community too, as it has already been installed more than 400,000 times. In 2021, we added new trading instruments (including many new cryptocurrencies, among them a few classic altcoins like Bitcoin Cash and Ripple, as well as national currencies like the Mexican peso and the South African rand) and raised the leverage for all our cryptocurrency pairs from 1:10 to a more competitive ratio of 1:25.

Furthermore, OctaFX upgraded its copy trading option’s rating and risk calculation system, providing a better, more elegant user experience. Receiving the ‘Best Forex Copy Trading Platform’ by FxScouts two years in a row (2020, 2021) is a testament to this progress.

Also, the 2022 launch of a 24/7 crypto trading schedule and – as alluded to above – the addition of 25 new cryptocurrency assets to its trading pool has raised the ability for us to stay competitive in an ever-changing and innovative blockchain market.

Our customer support handled 3.5 million client chats this year. We have improved, simplified and accelerated the operation of this essential service with the aid of upgraded artificial intelligence.

To illustrate this, the new system helped to close over 30,000 requests without a support agent, contributing to the company’s ability to interact with its clients in real-time.

Education still the key to success

Where would financial sovereignty be without its most beneficial asset? The company openly affirms that education is one of the core values it wants to expand and increase. In order to do so, OctaFX initiated the ‘ask to bid’ as well as the ‘learn to trade’ YouTube shows in India. While both feature Indian celebrities, the latter gave newcomers the opportunity to learn the art of trading alongside their favourite rookie celebrities. Both educational shows have garnered positive feedback from participants.

The company openly affirms that education is one of the core values it wants to expand and increase

We managed to increase our average of organised online events to over 50. Having installed courses in English in several African countries and the ones in Spanish in Mexico shows the spreading geographical reach of our financial training webinars and popular OctaFX Q&A sessions. The financial expert and trading specialist Manesh Patel has excelled in these kinds of high-quality sessions, by offering them in Hindi.

CSR as a ‘badge of honour’

Since its inception, charity and humanitarian aid have always played an essential role in our corporate organisation and activity. Some of the most crucial partnerships that assisted OctaFX in providing essential humanitarian support were accomplished with the Hemkunt Foundation. Among them was a project to distribute medical equipment to hospitals in Delhi, Gurgaon, Mumbai and Bangalore – in times when the COVID-19 pandemic was at its most rampant.

Another undertaking was the support for the construction of an educational centre in Khandwa, Madhya Pradesh. That way, the local community received a place for vocational training that is able to house up to 1,100 participants. Together with the projects from other Asian regions, 15 independent humanitarian initiatives in the course of the past year alone were erected.

New frontiers

The company expanded its reach and profile as a mere broker, already proficient as an innovative and trustworthy player in the investment industry, to growing into a comprehensive investment partner this year – helping every participant of its services reach their investment goals.

We endeavour to stand shoulder to shoulder with our clients, enduring the ups and downs of the market, helping individual growth by sharing vital information, and collaborating with the industry’s best educators and experts. They have unveiled their most inspiring stories with the OctaFX community.

In India, OctaFX managed to capture the ‘Best Forex Broker India 2021’ award and the ‘Best Forex Broker Asia 2021’ award by Global Business Review Magazine and Global Banking and Finance Review, respectively.

These awards recognise the major achievements we continue to make, improving the product, making it better, simpler, and more convenient – the way the customer demanded it to be. An exciting and ever-evolving learning curve appears to have materialised between us and our trading community in India.

One that helped both sides to develop a more intricate investor mindset and a deeper analytical approach: a strong investment strategy. India – as a key Asian and world politics player – is on the brink of important and unique economic developments, for which the OctaFX team continues to express deeply rooted enthusiasm to be part of.

Despite the double shock of the COVID-19 pandemic and raging global inflation, momentum from the Islamic finance industry has stepped up – again. While GCC countries are the most important movers, Islamic banking is gaining traction in Malaysia, Indonesia, Turkey and Pakistan. Despite the extreme adverse environment last year, global Islamic assets grew by 10.6 percent in 2020. This figure is expected to increase in 2022. With an estimated 1.9 billion Muslims around the world – nearly a quarter of the world’s population and the largest religious group in the world – the opportunity and necessity of Islamic finance is irrefutable. World Finance secured an advanced briefing from company managing director Robert Hazboun, who gave the low-down on their plans in an exclusive interview.

Did the pandemic change the business model of Islamic finance in any way?

We think so and in a positive way. COVID-19 showed how any bank’s ability to transition its business online is vital for survival. Digitisation and fintech collaboration for Islamic banks increases resilience in more volatile situations and provides new growth. Digitalisation is a priority. We believe the three aspects enhancing the industry’s resilience are digital banking services, issuing sukuk on a digital platform using blockchain technology, and improving cyber security.

Though the pandemic saw broad-based and revolutionary growth, we feel the sector has yet to fully take advantage of inclusive standardisation and the potential to grow sustainable financing. This is exciting and energising.

How do the drivers of Islamic finance compare to three years ago, pre-pandemic, in your view?

Gulf News has reported that the global trend of increased ethical consumerism is driving the appeal of Islamic products. We agree 100 percent. Also, the emergence of Islamic fintech is now driving the popularity and awareness of Islamic finance. According to IFN Islamic Finance, the UK has 27 Islamic fintech firms, followed by Malaysia with 19, and the UAE with 15, at least. This demonstrates the industry’s importance and potential. So, while the Islamic finance industry is steadily growing, even taking some hits along the way, its primary growth drivers remain solid. Even digging deeper roots. Our industry has huge potential to disrupt the global finance and banking sector – but in a very positive way.

Our service and software are about an on-going relationship that is cost-effective and long term hassle-free

What about demand from millennials and a younger generation?

We’re definitely seeing more demand from a younger generation. Millennials make up a big percentage of Islamic banking customers, which means they direct the growth and shape of the sector. This is supported by a study conducted by Alvarez & Marsal Middle East, which predicts younger generations will contribute to around 75 percent of banking revenue in the region over time. Many of our customers strongly attract millennials and the younger generation by offering innovative digital products and services, specifically catered to a young audience. Islamic banks must properly understand what’s relevant to the younger generation though, to attract and keep them as customers. This underpins understanding and trust in Islamic financing solutions. We feel it’s a win-win, ultimately.

What areas of Islamic banking promise to unlock the greatest innovation?

Although innovation in technology can be lower for Islamic banking compared with conventional banks, we’ve seen many of our customers dive deep into digital technology – many are early tech adopters and demand high levels of technological creativity. Similar to conventional banking challenges, Islamic banks face the same competitive challenges from fintech and tech disruption. Islamic banks must reimagine their way of doing business through innovation – they have no choice here. We feel there are no limits to reimagining an Islamic bank model that cooperates with a diverse group of partners. The bottom line is that Islamic banks have a once-in-a-lifetime chance to build an open banking environment supported by a modern, tech-savvy platform. We are here to support this, absolutely.

Product in brief

Deployable for a full-fledged Islamic bank, or as an Islamic window for conventional banks with a spread of configurations

Document Management System (DMS) for a fast, accurate document flow

Based on AAIOFI and IFSB standards with capability for local intellectual standards and Shari’a regulations

Powerful product building tools through parameterisation and Business Process Management (BPM)

Constant interaction with the customer during processes via omnichannel touchpoints

Fully supportive of robotics, AI, and digital coverage technology plus cloud availability to reduce costs

What role will ICS Financial Systems play here?

We have watched our customers grow and transform their businesses into digital-driven financial institutions. We are the core player in this field, committed to providing our customers with the most novel, tech-savvy, out-of-the-box products and services available, anywhere. Nothing has changed there. What has changed though is greater recognition that real value is about better productivity, or the peace of mind of free and on-going upgrades.

First and foremost, our service and software are about an on-going relationship that is cost-effective and long term hassle-free. That’s genuine value, we say.

How flexible is your software, particularly with regulation and cloud-based tech issues?

Our software is 100 percent fully digital, giving our clients full international standards, real-time business processing, and capabilities for tailoring their products on-premises, hybrid, or in the cloud. Our tools develop and evolve constantly to ensure our software can future-proof our customers’ activities across a range of banking capabilities that enrich the customer journey without compromise.

We know implementing new tech can often run up against old or new regulations. Therefore, we always work to ensure we have solutions that monitor processes in real-time, in case of potential problems or compliance issues, or even threats. All this means ICS Financial Systems supplies a standard of agility and digital excellence that other systems are judged by. We are confident about saying such a statement.

How close, or far away, is an interconnected Islamic global finance ecosystem, would you say?

We don’t see a global interconnected legal and regulatory framework for Islamic finance yet. The regulatory regime that governs Islamic financial institutions also differs greatly between countries. We strongly feel that Islamic finance serves the same foundation of ethical systems, wherever it is used, thanks to Shari’a Islamic instruments and concepts preserving and supporting Islamic economic behaviour. However, many international organisations have now been formed with the goal of establishing standards to enhance and standardise regulations. This is extremely encouraging to us and augurs well for wider acceptance.

Are there enough skilled professionals who understand Sharia-compliant products?

Unfortunately not. There is a lack of skilled professionals, which is why there is a huge demand for skilled professionals in Shari’a compliant products across so many jurisdictions, still. Thankfully our Islamic banking team is highly skilled with all the necessary Islamic banking certifications. We have always invested heavily in training and education and we continue to do so.

In focus:ICS Banks Islamic prime is an award-winning software suite designed not only to cover all Shari’a banking needs but to offer new levels of customer banking efficiency.

Three key features:

Its know your customer (KYC) feature means it maximises productivity and cost-effectiveness across all banking operations

Smart software solutions deploy cutting-edge tech like chatbots, cash management system (CMS), cardless payments and agency banking

It supports all known and approved Islamic instruments and their variants with in-built flexibility for an extra competitive edge, whatever the jurisdiction

What Sharia-compliant cloud banking features are your clients increasingly relying on and demanding?

ICSFS believes that in order to be truly digital, an Islamic bank must re-engineer the way it does business. All banks face growing competition from fintech start-ups and tech giants, with endlessly disruptive innovation. From early on, ICSFS had the foresight to capitalise on digital banking, providing a cloud platform that caters to each customer’s individual and bespoke needs, from digital-only Islamic banks and micro-finance to hybrid and cloud solutions.

What about other big-demand areas?

Although most of the Shari’a-compliant cloud banking features continue to be well utilised, we are now seeing a big demand for digital KYC, customer onboarding, blockchain, AI and robotics. We add to this list, customer account management, open APIs and loan originations. There are many other examples, too many to list here.

The platforms can be cloud-native or cloud-agnostic. Social engagement to financial inclusion are new business challenges. It’s a very diverse ecosystem out there. Lastly, we also never forget that organisations need a cloud computing solution that helps deliver corporate banking services such as wealth management services to their customers’ demands, but without significant burdens in expenditure. That is a given, always.

For any nation, industrialisation is the bedrock of job creation, poverty alleviation and economic growth. As Nigeria’s foremost development finance institution (DFI), Bank of Industry (BOI) has the mandate of financing the country’s emerging industrial sector. By providing long-term financing and counter-cyclical loans diversified across industries, the bank plays a central role in the country’s socio-economic development.

This is critical at a time when the country is determined to diversify revenue sources and improve economic output to spur the growth of other sectors like building and construction, manufacturing, agriculture and renewable energy. In fact, there is a broad consensus that for Nigeria to attain long-term prosperity, it must reduce its overdependence on the oil and gas sector that remains volatile and has repeatedly plunged the country into recessions when global oil prices decline.

To achieve the goal of being the heartbeat of industrial development in Nigeria, BOI has been building a formidable capital base in recent years. In the past five years, the bank has raised over $3bn from the international debt market. These include a $750m syndicated medium-term loan in 2018, a $1bn syndicated loan in March 2020, a $1bn syndicated loan in December 2020 and a €750m ($787m) senior Eurobond in February this year. BOI was the first African DFI to successfully issue a senior Eurobond, which was also oversubscribed.

We have already put plans in motion to visit the international market again shortly as the COVID-19 crisis gradually begins to ease out. The overwhelming interest from our international investors over the years is a clear indication of their confidence in the ability of the bank to deliver on its development-financing mandates.

A helping hand

By building a strong capital base, BOI today has strengthened its financial capacity to lend to the real economy. Since 2017, the balance sheet size has grown from $1.7bn to $4bn as at December 2021. During the year, the bank posted an impressive 75 percent increase in profitability to $151m from $85.8m in 2020.

Having a strong capital base not only means that the bank is well positioned to promote Nigeria’s industrial growth but also ensures that the bank continues to be highly rated by global rating agencies. BOI’s ability to raise funds in the international debt markets has, to a large extent, been supported by both its strong ratings and support from both the Central Bank of Nigeria and the Federal Government. Last year, Fitch affirmed the bank’s long-term issuer default rating at ‘B’ with a stable outlook. Moody also affirmed BOI’s long-term issuer ratings of B2 and changed its outlook from negative to stable.

BOI continuously strives to work with key partners towards improving job creation opportunities and alleviating poverty. Though a public institution, the bank is a limited liability company. This gives the bank autonomy and shields it from undue interferences. Since BOI was reconstructed in 2001 out of the Nigerian Industrial Development Bank that was incorporated in 1964, it has supported enterprises across several sectors like agro-processing, creative industries, engineering and technology, fashion, renewable energy, healthcare and pharmaceuticals.

BOI also offers products that specifically target the youth population. The Youth Entrepreneurship Support Programme, for instance, is solely aimed at addressing the worrisome phenomenon of youth unemployment in Nigeria. The product is designed to encourage young minds and fund their business ideas. It also equips young people with the requisite skills and knowledge to be self-employed by starting and managing their own businesses.

In the past six years, BOI has disbursed about $3.57bn to over four million enterprises, thereby creating over seven million jobs. It is worth noting that the bank’s support for micro, small and medium enterprises (MSMEs), which are the engine of the economy and job creation, has been phenomenal. During the period, a total of $861.9m has specifically been directed to MSMEs. The impact has been the creation of about four million direct and indirect jobs.

A platform for growth

BOI recognises that operating in a country where poverty is still prevalent is a herculean task. It is for this reason the bank is implementing its 2022–24 medium term strategic plan titled ‘Sustaining Purposeful Growth.’ The plan is designed to build a stronger and more resilient bank. But most importantly, it serves as a guide to increase its impactful lending, particularly in sectors like agriculture, manufacturing, infrastructure, export and import, and real estate among others that will define Nigeria’s future that is bound to be characterised by less dependence on oil and gas.

As part of our strategy, the bank recently launched the Growth Platform, Africa’s largest executor of MSME interventions. The plan enables BOI to partner with governments, international organisations, private sector players and non-governmental organisations to execute large-scale programmes that support the growth, development and recovery of businesses and households at different stages regardless of existing limitations. Through the platform, BOI is leveraging emerging technologies like big data analytics, agent networks and financial tools to profile and fund over four million Nigerian enterprises. So far the bank has managed to deliver $472m worth of interventions through the platform.

In the past six years, BOI has disbursed about $3.57bn to over four million enterprises, thereby creating over seven million jobs

While availing credit and grants has been critical, the platform has been instrumental in driving financial inclusion. BOI recognises that bringing more people into the formal financial sector is one sure way to combat poverty. This is important for Nigeria, where approximately 60 percent of the rural population does not have a formal bank account. The fact that the platform has facilitated the creation of over one million mobile wallets and opening of about 350,000 bank accounts demonstrates the bank is on the right track in terms of increasing financial inclusion.

Sustainable strategy

As a DFI, our operations are based on global best practices. The bank recognises the challenges facing society and incorporates them in its efforts in championing the development on all fronts. As a result, BOI has incorporated sustainability in its operations. One of the bank’s operating principles is supporting enterprises with the potential to be profitable, competitive and sustainable and have substantial developmental impact. For BOI, the sustainability strategy is anchored on transforming lives and enterprises responsibly through sustained interventions in economic development, environmental protection, social impact, ethics, governance and partnerships. The ultimate goal is to improve the world for future generations.

As part of its role in securing the future, the bank ensures that the enterprises it supports do not engage in activities that are detrimental to the environment or to the cohesion of the society. BOI has fortified its commitment to sustainability by becoming an official signatory to the UN Principles for Responsible Banking. The Principles are the leading framework for ensuring that banks’ strategy and practice align with the vision society has set out for its future in the UN Sustainable Development Goals and the Paris Climate Agreement.

A network for change

Though being a homegrown DFI, BOI operates in a market that is competitive and Nigeria has become a preferred investment destination for other global DFIs. This is evident given that in July of last year, G7 DFIs and multilateral partners committed to investing over $80bn in the private sector in Africa over the next five years. Apart from global DFIs, the local commercial banking industry has also demonstrated its interest in funding the real economy. While BOI recognises that it cannot reach all of the 40 million enterprises in the country, the bank currently deploys technology to broaden its scope and serve enterprises more efficiently and effectively. Through this, we offer end-to-end processes and field infrastructure for transparent profiling and delivery of financing to MSMEs.

The bank is able to achieve this through a network of 22,000 field agents, leveraging the power of digital identity and biometrics including extensive data capture, partnerships and integration with financial institutions and fintech platforms. In particular, working with fintechs, a flourishing industry with over 200 active fintechs, BOI has been able to explore new areas of opportunities for enterprises in areas cutting across payments, savings, e-wallets, remittances, mobile and online money services, wealth management, merchant services, card business, investments, and insurance among others.

Garanti BBVA has continued to enhance the outstanding range of products for its customers, even as the pandemic presented challenges. Personalised solutions and a rich product range have been instrumental in boosting Garanti BBVA’s cash and non-cash loan portfolio. Garanti BBVA constantly improves its business model and processes with operational excellence a priority. In order to accelerate and strengthen value creation, the bank continues to reach more customers by being present wherever customers are. As of March 31, 2022, Garanti BBVA has more than 21 million customers and 18,500 employees. It has a wide distribution network, with 861 domestic branches, eight foreign branches (seven in Cyprus and one in Malta), and one international representative office. The bank offers an uninterrupted experience and integrated channel convenience in all channels. It has 5,396 ATMs, the latest technological infrastructure, and an award-winning call centre. It also has internet, mobile and social banking platforms. For Garanti BBVA, data and technology are key elements in driving its strategy.

Since 2019, the bank has gained more than 3.1 million new customers and has reached more than 11.5 million digital and 11.1 million mobile customers. Digital sales have accounted for more than 80 percent of total sales. World Finance spoke with Ceren Acer Kezik, Executive Vice President of Retail Banking at Garanti BBVA, about constantly investing in technology, benefiting from advanced data analytics and artificial intelligence.

Garanti BBVA stresses financial health in its offering. What does it mean by this term and what is it doing for the financial health of its customers?

We define the concept of financial health as the ability to balance income and expenses by managing assets and debts correctly.

This creates the capacity to build some savings. This is the foundation enabling you to plan a free and secure lifestyle for the future. Financial health is very important in terms of realising life goals and taking appropriate action to achieve those goals. We think it is important to create a financial profile of each person, analyse their spending habits and raise awareness about their budget. We encourage customers to be prepared for unexpected expenditure and to build the capacity to save for future plans by better monitoring their financial positions.

In 2021, amid the pandemic and its uncertainties, challenges and the need for change continued. Individuals and businesses had to live with a new normal. For individuals, in addition to protecting their physical health, being able to manage their expenses and savings correctly became important focal points. Fortunately, the vaccine has curtailed the effects of the pandemic, and helped to restore and build optimism for the future.

One of the basic principles of Garanti BBVA is to offer easily realisable financial solutions to its customers anytime and anywhere with the best experience. The bank conducts monthly surveys to better monitor the needs of its users. This helps us address what is working for customers and to address any concerns they have. Armed with the findings of this research, we can enhance the experience for users and develop new products that will address customers’ needs.

As part of its policy of responsible banking, Garanti BBVA also communicates the advantages and possible risks of its products and services. In this context, it communicates transparently with its customers in sales and marketing activities and conveys all the information they need in a clear and easy-to-understand manner. It offers practical solutions and aims to establish long-term and sustainable relationships based on trust.

Can you share details of the progress on the digital onboarding process in Turkey? At Garanti BBVA, how did you prepare for this process and what did you do in the last year?

Compared with traditional methods, digital onboarding creates a fast, time- and location-independent experience for the customer. This process is also very valuable in helping banks to reach and serve more customers. It not only supports digitalisation to a great extent, but also facilitates the spread of digital banking services to more people.

While helping more people to access banking services, it also contributes to the growth of the sector and the economy. The most fundamental change for the banking sector in recent years has been the increase in the usage rates of active distribution channels and the number of digital customers. One effect of the pandemic was to encourage customers to use these channels more actively. The rate of transactions realised at the branch fell to between two and three percent, from the previous level of between five and six percent. Despite the increasing share of digital channels, branches are still an important part of our business. Garanti BBVA Customer Communication Centre aims to enhance the financial life of its customers by increasing the number of options.

Our innovation has led to a variety of alternative communication channel services for customers. With its customer-orientated approach, the bank aims to maintain its leading position in the sector in 2022. What we call ‘Contactless Onboarding Technology’ digitalises, end-to-end, key processes such as becoming a customer and applying for a credit card. It delivers a contact-free, easy and secure experience for customers. Completely digitalising the remote onboarding process, this step has been an important phase within the rapid transformation in banking triggered by the pandemic.

Increasing the individual services offered by the Customer Communication Centre, expanding the scope of the Smart Sales Management project and increasing the diversity and effectiveness of products regarding customer needs are among other goals. In addition, the end-to-end onboarding experience, the acquisition of more customers from digital channels and the dissemination and optimisation of our Live Support Service will be on the agenda in the upcoming period.

How do you position artificial intelligence in areas such as technology, customer service and digital banking? What are you prioritising in the use of artificial intelligence?

Technologies such as artificial intelligence and machine learning are tools that help us create more value for our customers and provide them with a better experience. These technologies change and develop over the years. However, we never lose sight of the fact that people are at the centre of everything we do. Therefore, it is important to use these technologies to accurately identify customer-based needs and to offer smart, personalised experiences and solutions. Today, while we offer almost all of our products and services through our mobile application with an easy experience, we observe that it is also important to be able to provide the human touch when required.

For example, while we enable our customers to find answers to their questions with our artificial intelligence supported smart assistant UGI, we also enable them to reach our customer representative directly from the mobile application.

By providing the balance between the digital ecosystem and the human factor, we focus on creating the relationship model of the future and establishing a trust-based relationship with our customers. Artificial intelligence helps to make the data collected with different algorithms more meaningful.

How does Garanti BBVA create value for its customers, employees and stakeholders? What are you doing to add value to society? What are the main company values that determine the way the bank conducts its activities?

Garanti BBVA shapes its products and services in a customer-centred manner acting with the guiding principle that ‘the customer is our priority.’ This principle underlines the banks’ customer-orientated approach. Everyone who works at Garanti BBVA knows the importance of understanding their customers. As part of a strong commitment to responsible banking, we comprehensively share information with our customers. We also respond to customer needs with a results-orientated approach.

Garanti BBVA’s corporate culture includes innovation by valuing the opinions of its employees, who are encouraged to put forward ideas that will improve the customer experience. In every area, staff inspire their colleagues with the work they do. Garanti BBVA staff focus strongly on meeting customers’ needs. But they go the extra mile to find solutions to exceed customers’ expectations. Fostering Garanti BBVA’s work culture, our ‘One Team’ value encompasses employee collaboration, the importance of commitment to work, and the sense of responsibility that needs to exist in order to achieve the ‘common purpose.’

Garanti BBVA communicates with its stakeholders regularly, and attaches great importance to listening to their ideas. Garanti BBVA is an inclusive, forward-looking bank for all its stakeholders, in all areas.

Can you share your perspective and your goals for sustainability? What kind of products and services does Garanti BBVA offer to its retail banking customers as part of its sustainability efforts?

Garanti BBVA is taking a lead in sustainability to positively influence customers, decision makers and the sector. The bank strives to raise awareness of sustainability among stakeholders and the wider community. The bank has been working on sustainable development and the fight against climate change for 15 years. This is one of the bank’s strategic priorities. Garanti BBVA draws on its sector-leading know-how and experience to drive sustainable development in the market. Its business model embraces the opportunities stemming from sustainable development as well as climate change-related risk management. In 2020, together with the BBVA Group, we have made sustainability a strategic priority. While contributing more than $810m to the sustainable finance market, we increased the number of our products and services in the field of sustainable finance to 50.

We have achieved a major transformation in our business from both an environmental and social point of view. By expanding our sustainable range, we have also contributed to our country’s economy. We have invested more than $3.8bn in sustainable development. In March 2021, Garanti BBVA became the first bank in Turkey to announce that it will not finance coal and coal-related activities. The bank said that it will not finance new investments in coal-fired power plants and coal mines. It will eliminate its exposure to any investment in coal in its portfolio by 2040 at the latest. The bank has been the first and only Turkish signatory to the net-zero banking alliance. It is committed to align its portfolio with the net-zero emissions target by 2050.

In addition to green loan and gender loan, the bank offers its customers the rooftop solar power system (SPS) shopping loan for using solar power in their buildings and the environmentally-friendly building insulation loan for supporting efficient energy consumption in buildings and promote insulation investment. It also offers the corporate green auto loan, the first of its kind in Turkey.

The bank intends to lead the transition to more efficient hybrid and electric vehicles at advantageous low rates on the one hand, while contributing to the world’s future by encouraging replenishment of fleets with environmentally-friendly vehicles on the other. Based on its contribution to the environment and the quality of human life, we have offered a new shopping loan opportunity to encourage the use of electric bicycles.

Three Garanti BBVA Asset Management mutual funds with a sustainable theme raised money in 2021: Garanti AM Clean Energy Variable Fund, Garanti AM Sustainability Equity Fund and Garanti AM ESG Sustainability Fund Basket Fund.

We regularly organise events to communicate our sustainability strategy and we also run programmes to boost our staff’s knowledge of developments in sustainability.

For BA Glass, sustainability is a core concept and one that enters into all aspects of life and human need. Sustainability for us is about having a green mindset every time we design and produce a glass container. As a company, we have been following an eco-friendly path year after year by carrying out actions and initiatives that allow us to reduce our impact on the environment and safeguard future generations.

For us, sustainability begins in our products. Given its unique properties and composition of natural materials, glass is infinitely recyclable. When we choose food and beverages in glass packaging, we choose to protect the health, not only of individuals and society but also of our planet. At BA Glass, our sustainability strategy is based on six pillars: customers, consumers, shareholders, people, environment and society – which allow us to ensure economic and social development as well as to protect the environment.

We have been developing initiatives that will help us to take a step forward towards a more sustainable future

After an impressive recovery in demand for glass packaging following the COVID-19 outbreak, we are facing a very challenging moment due to an unprecedented increase in energy costs, which is affecting the energy-intensive industries. The incentive to decarbonise the industry was reinforced and, at BA, we continue to develop our carbon reduction roadmap with the aim to achieve carbon neutrality by 2050.

We pursued our commitment to the Science-Based Targets initiative (SBTi) that promotes CO2 reductions. As part of this initiative, we are committed to a 50 percent reduction in CO2 emissions per tonne of glass produced, by 2035. And in just one year, we were able to reduce these emissions by 15.9 percent (scope one and two of SBTi criteria).

At the Porto Protocol event, we have made public our commitment to respect and protect the environment, through many different goals, such as reducing the use of natural gas and increasing the use of energy from renewable sources. Therefore, we have been developing initiatives that will help us to take a step forward towards a more sustainable future. Following our plan, in 2021, we built a third photovoltaic park, which is on the roof of our Plovdiv plant. And we achieved a share of 86 percent of renewable energy in the total electricity we used in 2021.

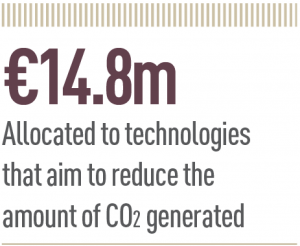

The ambition to become carbon neutral requires a major technological disruption in the industry regarding melting technology. Our shareholders already allocated €14.8m to the development of technologies that aim to reduce the amount of CO2 generated and its capturing and reuse, through R&D projects.

The development of a hybrid furnace is one of the projects where we committed several resources with the aim to switch from natural gas to renewable energy. Preserving and respecting the environment is part of our business strategy and so our commitment to the environment goes further and further.

Through the Glass Seeds Project, BA continues to endeavour to hold educational projects for the youngest generations, promoting equal opportunities and meritocracy in the regions we have our plants. Based on four main pillars: foundations, work, future and planet, this project contributes to the development of leaders and citizens, as well as for a sustainable future.

A PURE focus on sustainability

And because we do not stop in our mission to green our industry, we have launched our own sustainable brand: PURE. More than just a glass packaging brand, PURE is about being immersed in nature. PURE is born from the unique mindset that brings innovation and sustainability together in one brand, where nature comes first in every stage of the process. With PURE, we produce food and beverage containers that are sustainable from conception to delivery. Therefore, incorporating recycled glass into our products is a main priority, allowing us to extract fewer resources from nature and reducing CO2 emissions. Furthermore, we are constantly challenging ourselves to actively reduce the weight of our containers and again, in 2021, we reached a new record of the number of lightweight containers launched in the market.

At BA Glass, sustainability goes beyond what we do today. For us, sustainability is a long-term commitment that challenges us to reduce our impact on the environment, ensuring the future of the next generation. Sustainability comes within the glass, always!

The war in Ukraine has accelerated the need for a new energy system in Europe to reduce dependency on Russian oil and gas. This transition is going to require heavy investment in everything from renewable energy to energy storage, expansion of power grids and energy efficiency improvements. It is also going to raise demand for all the metals used in electrification, and the recent energy crisis has shown how dependent we still are on fossil fuels like oil and gas during a transition period.

In our Global Theme portfolio, where we gather our thematic investments, we have had exposures to renewable energy, the energy transition, natural resources and smart materials for some time. These kinds of exposure are even more top-of-mind in this situation. Batteries are another hot area of investment. High commodity and materials prices and the accelerating energy transition are making the segment even more interesting, as initiatives are likely to increase.

Battery investment opportunities

Electrification of the vehicle fleet is pivotal to creating a sustainable energy system, since greater prosperity usually leads to increased transport. Emissions from combustion engines are no longer declining and customers are showing a preference for larger cars. Aimed at reversing the emissions trend, the sector is in the midst of a historical transition that involves massive investment. Battery power has taken a big lead compared to alternatives like hydrogen.

There are plans for major expansion of battery manufacturing, but materials supply needs to be scaled at a similar pace

Batteries are also attractive for several other use cases, including heavy vehicles and stationary energy storage. Vehicles, especially passenger cars, are currently the biggest use case so far and are driving the battery market.

Battery-powered electric vehicles (EVs) are going to take over the automotive market, at least if the actions of carmakers and the financial market are anything to go by. American Tesla has the fifth-largest market cap in the world. Likewise, the American Ford Motor Company’s stock rose a full 150 percent in 2021 when the electrified F150 pickup was launched before Tesla’s Cybertruck. Leading traditional car manufacturers are investing heavily in electric power, even though they are not major players in the segment. The further development of combustion engines is being phased out.

In 2021, 6.6 million fully battery-powered passenger cars were sold globally, up by 120 percent from 2020 according to Bloomberg NEF (see Fig 1). So far, this is only a fraction of the total market of about 70 million passenger cars in 2021. Tesla’s volumes grew by an impressive 70 percent, in spite of component shortages. The total market in China has doubled in size in a single year. Domestic manufacturers dominate – but the market is suffering from fragmentation and weak profitability, which has made Chinese automotive equities volatile.

The most exceptional thing about Tesla is not its growth (Chinese electric vehicle manufacturer Xpeng grew by 275 percent in 2021 compared to 2020), but that Tesla has high and rising margins. The company is actually reporting a higher profit margin right now than quality leader BMW ever has. This has intensified focus on Tesla’s integrated business model, where not only software but also batteries are developed internally. Parallels are being drawn to Apple’s strategy in mobile phones, which explains why the valuation is so high.

Earlier forecasts talked about growth for all-electric vehicles of about 30–40 percent a year until the end of the decade. When the technical shifts really take off, however, it is tricky to make forecasts and growth could be underestimated – as mentioned, the growth rate was considerably higher in 2021.

Bottlenecks set limits

The battery is the most expensive component in an EV and costs the car manufacturer about SEK 100,000 ($10,000) to buy, for 70 kWh capacity. Huge technical advances have been made and the cost per kWh is a fraction of what it was in 2010. Many believe that demand for EVs will be driven by lower prices, especially for batteries. At present, however, we are seeing steep price upturns for the battery metals lithium and nickel, making both batteries and EVs more expensive.

Batteries use some materials that have never been mined on a large scale before, especially lithium. There are plans for major expansion of battery manufacturing, but materials supply needs to be scaled at a similar pace. This is a significant challenge, which is likely to be overcome with time but will create different cycles in the chain. At present, semiconductor shortages are constricting the supply of products including EVs more than battery supply.

This has already, for instance, meant that Tesla failed to launch products at prices as low as it intended. One explanation is that high expectations for EV range require bigger batteries. For the Tesla Model 3, range differs 30 percent between trim levels (versions), with a longer and shorter range respectively (the price difference is 12 percent). In addition, both trim levels have been upgraded with larger battery capacity. EVs are still premium cars and rapid price drops cannot be expected. Driving characteristics are pushing demand and subsidies are helping. At present, however, charging stations are still too few in number – a huge expansion is required here.

China dominates

The car battery market is currently dominated by Chinese CATL, Japanese Panasonic and the South Korean companies LG Energy and Samsung SDI. Minor players like the Chinese EVE and Svolt have aggressive investment plans. A Swedish company, Northvolt, will begin production this year.

The growth rate for battery manufacturers basically tracks EV volumes with additions for increased battery capacity and subtractions for price erosion. 2021 was exceptional, with 100 percent growth due to the post-pandemic recovery and strong EV market. The market is tough, with expectations of constant efficiency improvements and heavy investments. Strong partnerships between battery and car manufacturers have become common to avoid under- or overinvestment. These agreements improve the battery manufacturers’ potential to achieve high capacity utilisation while securing volumes for the carmakers. But shared risk-taking can also reduce the battery manufacturers’ ability to boost margins when demand is strong. The car manufacturers take volume and price risks and must correctly forecast their market shares. Selecting a better battery technology than the competition is also important, of course.

The transformation of the power system is creating increasingly stronger incentives to invest in stationary energy storage

Chinese CATL is now the leading independent battery manufacturer, with high growth and profit margins. CATL has also been successful with both Chinese and foreign manufacturers, partly by having the capacity to offer different types of batteries. CATL’s sales this year are expected to be four times higher than in 2019 and the company has the biggest expansion plans in the sector. The share has been rewarded with high valuations.

LG Energy executed a highly sought-after IPO in late January and is building an even larger battery factory in partnership with GM in the US. Panasonic has mainly been a supplier to Tesla, which has driven the trend. Tesla and Panasonic are not as transparent about their capacity plans as other manufacturers. On Tesla Battery Day in 2020, the company stated production targets of 100 GWh for 2022 and 3,000 GWh for 2030.

Technical advances with new materials

Car batteries for EV operation consist of thousands of linked cells. Packaging them in a smart way can give car manufacturers a competitive advantage. Better packaging has compensated for the lower density of the LFP battery chemistry. Building the vehicle chassis where the battery cells have a structural function is another efficiency improvement initiated by Tesla. Processes to bypass energy-intensive furnaces have tremendous potential to reduce costs and environmental impact. Acids with lithium salt are currently being used as electrolytes. Research is in progress to replace such fluid electrolytes with solid state ceramic materials that produce higher energy density and reduced leakage and fire risk. The listed US company QuantumScape has carved out a profile here, although the company currently has no revenues. The market leader CATL and the Indian Reliance are studying sodium as a low-cost alternative to lithium. In addition, sodium-based batteries can be charged quickly.

Next market: Stationary energy storage

EVs are currently dominating the demand for large batteries. Meanwhile, the transformation of the power system is creating increasingly stronger incentives to invest in stationary energy storage to compensate for fluctuations in production. In particular, the shortage of natural gas has driven European electricity prices up by several hundred percent. Storage imposes different demands than EVs: A low price per charge is critical, while weight and size do not matter much. Both markets use similar batteries today, but the stationary market is going to be driven towards cheaper materials. The segment is going to rise when storage gets cheap enough that solar and wind power can compete with fossil energy sources, regardless of weather and demand. The market is in its infancy. Examples of equities with dedicated exposure are Fluence (US) and Freyr (Norway/US). Private individuals can also benefit from stationary storage in connection with power cuts or take advantage of cheap electricity hours – Tesla launched the lithium-ion powered Powerwall 2015 and has sold more than 250,000 units.

Investment opportunities

The balance of power is going to change as the journey continues. This should also be the point of departure for those who want to invest in the battery sector. Investors can choose among vehicle manufacturers, manufacturers of batteries and battery components, producers of the input commodities and companies involved in charging stations.

There is a lot to be said for using a specialised EFT to gain broad coverage in the battery segment, including equities in China and South Korea that can be difficult to trade in. An actively managed fund is preferable for profiting from sector dynamics. Carnegie Private Banking launched a discretionary portfolio, Global Stockpicking, this spring, which will be active in areas including this one. Some battery exposure is also gained through our Global Theme portfolio via thematic investments in smart materials and the energy transition. If there is one thing to be certain of, it’s an exciting time to be investing in the battery sector and there are plenty of investment opportunities for those focusing on the green transition.

International payments are fundamental to global trade and business as we know it today. Without an efficient cross-border transfer system, businesses and their banking partners stand to lose significant capital. Yet for decades, the day-to-day challenges of managing cross-border payments have plagued us. Delays, hidden fees, failed transfers, limited access and a lack of transparency throughout the chain have all contributed to making international transfers problematic and at times costly, slowing business and hindering relations.

In 2020, under the request of the G20, the Financial Stability Board created a roadmap to improve cross-border payments, with key targets including increased data quality, steps to coordinate regulatory frameworks and research into new and existing payment infrastructure. Yet issues still remain, and many banks and corporates continue to struggle.

At Bank of the West – a subsidiary of BNP Paribas headquartered in San Francisco – we’ve signed up to SWIFT global payments innovation (gpi) to help alleviate the most pressing of these challenges. The multi-year SWIFT gpi initiative has been rolled out in stages by the global banking community with one goal: to improve the cross-border payments experience for both senders and recipients. Thanks to greater end-to-end transparency, improved speed and the flexibility to cancel payments en route, this new service is a sought-after advancement in the global payments landscape.

Addressing a global need

Banks have long facilitated cross-border payments for their clients to enable international trade and business to thrive, but the process has often been overly cumbersome, slow and opaque. “Historically, clients have sent their cross-border payments through a black box, with no understanding of the full cost or the point at which funds would be credited to the recipient,” says Larry Feinberg, Head of Digital Payments for Corporate and Commercial Banking at Bank of the West. “Improvements to the cross-border payment experience are long overdue.”

Both banks and their clients have for a long time been subject to high costs and delays in transfers. This is partly due to the fact there are multiple parties – banks, market infrastructures and corporate businesses – required for the clearing and settlement of every cross-border payment.

Faced with these hurdles, pressure has been mounting for heightened transparency and a more streamlined cross-border payments system that minimises the number of intermediaries involved. This pressure has only been exacerbated by the exponential growth in cross-border trade, huge technological innovations and global events – all of which point to a clear need for faster payment solutions with better data around them.

Cross-border payment issues

Delays in recipients receiving the funds aren’t just an annoyance; they can lead to several complications, not least legal risk, according to Meghan Birmingham, Head of Transaction Banking for Corporate and Commercial Banking at Bank of the West. “Clients face legal and reputational risk when their vendors are not paid on time,” she says. “Timeliness and payment confirmation are critical deliverables for our clients.”

Cross-border payments often lack the certainty provided with domestic payments. Those delays can be especially costly for high-value payments, not least merger and acquisition transactions, where speed is critical. Without the ability to track statuses in real time and confidently confirm receipt of funds, we’re faced with several hurdles. Transaction costs can also be significant, especially for treasurers dealing with a high volume of cross-border payments. Fees can be high, and there’s often a lack of transparency around them, which can cause friction between corporates and suppliers. Intermediary fees deducted along the payments chain may be unexpected and lead to incomplete payments. In addition to this, exchange rates can be notoriously difficult to predict and can fluctuate unexpectedly, further adding to the problems.

Improvements to the cross-border payment experience are long overdue

The issue of transparency extends beyond just fees, too. In most industries, treasurers look to their bank to provide insights into the status of their cross-border payments. While banks are indeed well positioned to handle these inquiries – employing direct messaging with other SWIFT member institutions – this need for transparency places a significant burden on client service teams.

The lack of communication across the value chain can raise further costs for banks and their clients, while undermining corporate cash flow forecasts and ultimately straining relationships between suppliers and business partners. The challenges are multiple, and addressing them sooner rather than later is key.

The SWIFT Tracker

The aim of SWIFT gpi is to address these long-standing issues and to open the door to smoother, more transparent cross-border payments. Realising this potential requires all participating banks to be aligned in their goals and to adopt new, multilateral agreements that outline the business rules governing gpi services.

At Bank of the West, we have committed to doing exactly that. The rules are key to improving payment speed, increasing transparency around fees, enabling end-to-end tracking and helping to ensure remittance information remains unaltered throughout the payment chain. Fundamental to this transformation in cross-border payments is the SWIFT Tracker, a cloud-based solution for connecting all parties in the value chain.

This innovative technology enables significant enhancements in the speed, transparency and traceability of cross-border transactions. That’s helped in part by specifically focusing on the MT103 – a standardised SWIFT payment message used for cross-border wire transfers. The message includes all details about the transaction, including the date, amount, currency, sender and recipient, to help senders and recipients trace payments more easily and better manage their progress.

The key tenets

SWIFT gpi has four key goals. The first is making funds available the same day, provided they’re received before the recipient bank’s stated cut-off time. According to SWIFT, nearly 50 percent of gpi payments are credited to end recipients within 30 minutes, 40 percent in fewer than five minutes, and almost 100 percent within 24 hours. That makes the median processing time less than two hours (affected by various factors, including geographical location and the online hours of the relevant banks). It also depends on the number of parties involved; on average, cross-border SWIFT payments require only one intermediary between the sender and the recipient, making the process significantly quicker and more efficient.

The second goal is to ensure end-to-end payment tracking and confirmation is readily available throughout the process and with every transaction. Since the end of 2020, it has been obligatory for all gpi banks to provide final confirmation of payment for every MT103 message sent on the SWIFT network.

This means both clients and banks are able to see if a payment has been credited to the end recipient, or if it has been rejected or transferred outside of the network. The introduction of a new, unique end-to-end transaction reference (UETR) makes the tracking experience highly intuitive – much like how today’s parcels are tracked in real time and updated with locations, time stamps and delivery details. At Bank of the West we’re able to log in to the Tracker to check the payment status, which helps us improve liquidity management. It also helps us identify problem areas and to implement better service-level agreements as well as to see other gpi banks’ adherence to those SLAs.

In addition to this, the gpi tracker aims to improve transparency around fees throughout the payment chain, including any deductions against payment amounts and applicable exchange rates. It also aims to ensure the integrity of data provided by clients regarding their payments, providing insight into the purpose of the transactions.

As a further benefit, clients are also able to use the Stop and Recall service to electronically recall transactions immediately if an error has occurred or if fraud is suspected, streamlining the cancellation process. This can be done regardless of what stage the payment is at in the chain, as the recall request – initiated with the original UETR transaction reference – is directed to whichever bank is currently in possession of the funds. All of this is made possible by the ability to track payments in real time, allowing quick, easy access to cancellation data via multiple channels.

Harvesting the potential

Through collaboration with member banks and corporates, the SWIFT gpi program aims to remove friction points that have long persisted for cross-border payments while further extending connectivity between different markets. By integrating data-rich ISO 20022 messaging standards, the technology opens the door to more value-added services for clients, making a payment’s status visible from the time it’s sent until the moment it is received by the recipient bank. It also enables clients to view real-time status and fee information without having to rely on the bank’s client services team to investigate payment delays and fees.

“SWIFT gpi brings essential information to customers when they need it – immediately,” says Feinberg. “The information provided by gpi is not only transformational – it’s necessary.” The pandemic has shown the value of international collaboration, and that must extend to the banking and corporate world, too. It’s solutions like these we need if global trade and business are to continue to thrive in the face of future challenges.

The Manises Department of Health provides public healthcare, both outpatient and at home, to more than 199,000 people in the Valencia region of Spain. We provide healthcare services at 14 locations including the Hospital de Agudos de Manises in Valencia city, 10 healthcare centres, 10 local clinics, two speciality centres and the Hospital de Crónicos in Mislata. Since its creation in 2009, the Manises Hospital has boasted a professional team focused on safe and high-quality healthcare. In terms of accessibility, quality and level of care, as well as corporate reputation, we rank among the best public hospitals in Spain, according to the consultancy firm Merco’s Health Reputation Monitor report.

Scientific evidence has shown, for years, how the health of the planet is directly related to the health of its people. As health specialists, we are aware that we can only improve the health of citizens with a comprehensive approach in line with the World Health Organisation’s ‘One Health’ strategy. Based on this principle, we have drawn up our own sustainability strategy focused on attacking the risks that atmospheric pollution, climate change and biodiversity loss can have on the health and wellbeing of the population.

The Manises Health Department has been committed to sustainability since it was founded in 2009, adopting an approach that integrates the health of the planet with the health of the citizens of Valencia. We were one of the first large healthcare organisations to officially commit to the Science Based Targets initiative (SBTi) to reduce our carbon emissions and prevent the effects of climate change.

Range of measures

Since the beginning we have invested in a plan to improve the energy efficiency of our facilities. We have implemented a wide range of measures as part of the plan, cutting our consumption of natural gas by 51 percent since 2013, our consumption of electricity by 30 percent since 2013 and our consumption of water by 20 percent since 2018. Infrastructure improvements have been key, but so has the reduction of plastic and paper waste.

Together all these measures have enabled us to bring about a 70 percent fall in our carbon emissions since 2013 (see Fig 1) and achieve energy efficiencies of 40 percent over this same period. Furthermore, 67 percent of our energy is from renewable sources. To put this in context, the European Commission’s Green Pact calls for the EU as a whole to increase energy efficiently by 32.5 percent and have at least 32 percent renewable energy in its energy mix, both by 2030. We have also reduced our paper, cardboard and plastic waste, cutting the latter by up to 70 percent over the last five years, going from 5,780kg in 2015 to 3,420kg in 2021.

All of this would be impressive for a private company but is all the more so given that we are a public-private health provider, with many of our facilities open 24 hours a day, seven days a week, 365 days a year. It demonstrates the crucial role that careful management can play in supporting the health of both people and planet and motivates us to continue on our path towards sustainability.

We save energy through a heat recovery system, variable flow air distribution systems and high-efficiency boilers and air conditioning

Such measures are essential in the current climate, where rising commodity prices, the COVID-19 pandemic and geopolitical instability are putting those reliant on fossil fuels under increasing pressure. Improving our energy efficiency, reducing our consumption and improving our carbon footprint are not just good for people and the planet, they have offset the increase in the cost of energy, protecting our annual operating profits.

The management system at the Manises Health Department has been specially designed to enable us to continuously measure and improve our performance. It is audited and certified by experienced external institutions to a wide range of quality standards. Manises Hospital, in fact, has received more accreditations than any other public healthcare centre in the Valencian Community according to the Autonomous Registry of Quality Certifications of the Ministry of Universal Health and Public Health. These accreditations include the highest accreditation granted by the Institute for the Development and Integration of Health (IDIS) in 2020: the EFQM 500+ distinction. It is the highest distinction awarded by the Club for Excellence in Management (CEG) and the most recognised and widespread international quality management model in Europe. Furthermore, we are the only health department whose healthcare centres all have ISO 9001 and ISO 14001 certifications, for quality management and environmental management respectively. Manises Hospital also boasts the SENSAR safe hospital certificate.

The hospital building itself has a 300 sqm rooftop solar park that generates up to 12,000 litres of domestic hot water per day for self-consumption. It also has 250 photovoltaic solar collectors capable of producing 40 kWp of electrical energy. The extensive landscaped areas of the hospital grounds, which account for around 10,000 sqm of our 55,000 sqm footprint, are irrigated with the hospital’s own wastewater following treatment with reverse osmosis. Internally, we save energy through a heat recovery system, variable flow air distribution systems and high-efficiency boilers and air conditioning, as well as sensors for pumping, cooling and heating water.

Renewable sources

Since the implantation of the energy efficiency plan in 2018, the hospital has reduced its consumption of natural gas by 40 percent and saved 3.8 million kilowatts of energy. Renewable sources now account for 65 percent of the hospital’s energy use. Together these savings have enabled a reduction in carbon emissions of up to 43.5 percent. Going forwards, we have allocated a large investment for improvements to our building control system, which will allow us to achieve better energy automation, adjusting our energy demands according to different conditions.

It is unsurprising, therefore, that in October 2021 we were recognised for our commitment to the fight against climate change at the 38th National Congress of Hospital Engineering, a conference at which the engineering sector addressed the environmental development of healthcare centres. Manises Hospital was the first public hospital in Spain to be awarded in the ‘Climate Emergency’ category. Speaking at the conference, Iván Ruiz, Head of Infrastructure at the Manises Hospital, called the award an “endorsement of our contribution to the health of the environment and the planet.”

We hope that other institutions, both public and private, here in Spain and around the world, will follow in our footsteps when it comes to greening their facilities. It’s not just health care settings that could benefit – because it’s been largely through improvements to infrastructure and management that we have achieved our sustainability goals, these learnings could be applied to a broad range of buildings, from housing and hotels to shopping centres. It’s more complex when it comes to switching to renewable energy sources, as that depends on the national and regional context, but there are many localities where following our example is eminently possible. We are proud of leading this change.

It is surely the mark of a successful bank when it not only continues to provide services to customers through challenging times, but actually improves the quality of the offering. Now into its fifth decade of operation in the Hashemite kingdom situated at the very crossroads of Asia, Africa and Europe, Jordan Islamic Bank did just that during the pandemic.

Despite the difficulties, the group pushed through a digital transformation programme that introduced a whole new range of electronic banking services as well as a variety of other innovations. The highly successful ‘Islami Mobile’ and other Islami-branded products were taken several steps further through such services as electronic bank accounts, a self-registration capability, the ability to review the latest transactions in a variety of formats, enhanced payments, instant money transfers through an app called CliQ, an E-wallet branded JoMoPay, and payment of bills, among numerous other conveniences.

In this way Jordan Islamic Bank expanded during COVID-19 and the bank continues to strengthen digital services to keep pace with the latest developments that meet the needs of its customers in accordance with the provisions and principles of Islamic Sharia. As these services were expanded, so did the bank’s reach. Paid-up capital stands at $282.1m, an important statistic reflecting the institution’s strength. The number of active accounts hit 1,146,000, marking impressive penetration in a country of 10.3 million. The number of employees grew to 2,439. And the total of shareholders is approaching 11,000, with the share register bolstered by some of Jordan’s leading business figures and Arab national institutions.

A commanding lead

Today JIB, as the institution is popularly known, ranks first among the country’s Islamic banks and fourth among all Jordanian banks for assets, deposits, financing and investment.

During a busy 2020, the network of ATMs grew from 266 to 288 as the bank rolled them out right across the kingdom. Simultaneously, the number of machines that accept cash deposits, as distinct from just issuing cash, was boosted to a total of 67. And to help protect customers from the pandemic, JIB steadily replaced existing ATMs with technologically superior machines that accept contactless cards, a service in which the bank was a pioneer.

The bank continues to strengthen digital services to keep pace with the latest developments

Customers can pay for daily purchases and carry out deposits and cash withdrawals that accept the service without needing to touch the card reader or ATM at all. The transaction is done easily and securely under a pre-determined maximum limit to reduce any risk.

While improving the services available at its brick and mortar branches, JIB also made progress with its digital branch, a flagship project based on the latest financial technology. Today it is possible to do just about everything through the digital branch. Services range from opening an electronic account, instant issuance of debit cards, cash withdrawal and deposit, money transfers, applications for mobile banking, updating of customer contact information and, if the client needs help, it is even possible to get any problems sorted via a video call with highly trained staff. In other customer-friendly initiatives, a tool called ‘My Finances’ makes it easy for customers to check the state of their finances while ‘My Cards’ lets them track all transactions and limits.

Customer-orientated management

As JIB’s performance through the pandemic shows, the management team follows a practical, relentlessly customer-orientated approach. The website illustrates this approach. Written in jargon-free language, it presents the bank’s services in a highly accessible way.

The bank’s Chairman is Musa Abdel-Aziz Mohammad Shihadeh, general manager for 37 years before heading up the board. He holds an MBA from the University of San Francisco and a Bachelor of Commerce. As chairman or board member of a wide variety of companies involved variously in industry, trading, investment, education and insurance, he has his finger on the pulse of the nation’s economy.

Founding values

Both management and board adhere to the institution’s founding values. Namely, to meet the economic and social needs of citizens in the fields of banking, finance and investment in accordance with the principles of Islamic Sharia.

Thus transactions and contracts are subject to the supervision of a Sharia board composed of specialist scholars who ensure the integrity of all dealings. Underlining JIB’s commitment to Sharia principles and practices, the branding was overhauled some 18 months ago, with the word Islami prefixing the names of its electronic channels. Last year’s achievements follow on from the momentum built up in 2020. The ‘Islami Mobile’ app, an updated website, self-service kiosks, dedicated ATMs and an interpreting app for clients with disabilities: were all launched during 2020 to implement the bank’s digital transformation strategy.

Spoilt for choice

The range of personal services is unusually diverse. A full portfolio of Mastercard and Visa banking cards is issued including, in the case of the Mastercard brand, standard, titanium, gold, Al Baraka (blessing) and family prepaid. And helping to steer customers towards these tools through the digital electronic channels, JIB runs a rewards programme called ‘My Points’ under the Islami brand for purchases locally and internationally.

Similarly, a customer loyalty initiative gives shoppers a direct cash discount when they use one of the bank’s cards at approved merchants and stores.

Some of JIB’s most interesting products are what might be called lifestyle services. Getting married? The Zafafi package covers marriage costs such as hire of the venue and finance for furniture and other essential items for the home, even the honeymoon. Doing renovations?

Another package finances building work and wages through the Ijarah formula, a word translating literally as ‘to give something on rent.’ As these products show, flexibility is one of the bank’s watchwords. For instance, it accepts deposits in Jordanian dinar and foreign currencies in a wide range of accounts – current, demand, joint investment portfolios and savings.

Reflecting a national culture

True to its founding principles, the bank’s activities uniquely reflect the national culture. Available funds are invested according to Islamic modes of finance, for instance mudarabah, musharakah and ijara mawsufa among others. Variously, these products finance education, medical treatment, annual pilgrimages to Mecca known as the Hajj and Umrah, and the installation of renewable energy for individuals and companies. Other corporate-focused packages facilitate direct investment in shares and the purchase or leasing of real estate. JIB’s al musawamah card is an instalment product that complies fully with the provisions of Islamic Sharia. The cardholder uses the card at an approved merchant and the payment is made from the customer’s account without any profit margin. The limit is renewed by the amount of the monthly instalment paid, thus preventing any debt.

While JIB runs a full portfolio of retail products, it has not neglected the corporate sector. Among other in-demand services, it issues instant money transfers through Western Union, rents out safe boxes, provides letters of guarantee and letters of credit, and buying and selling of foreign exchange on a spot basis. The bank also acts as a broker on the Amman Stock Exchange through a subsidiary Sanabel Alkhair for Financial Investments, which buys and sells shares, investment certificates and other paper transactions on behalf of corporates.

Overall, the corporate portfolio adds up to an unusually broad range of finance services that encompass just about every element of the Jordanian economy. There are funding programmes for professionals, craftsmen and SMEs operating in such sectors as health, energy, environment, education and training, safety and occupational health, religious studies and related activities in culture, arts and literature.

Helping those in need

The bank assumes its social responsibilities and sustainable development through a charitable programme funded by donations and other forms of support. We proudly fulfil our duty to customers and the wider community. Among the many beneficiaries of the bank’s generosity are those with special needs, disadvantaged groups and the poor. Just one practical expression of this commitment is the Blind Card. Issued to people with visual impairments, it is part of JIB’s policy of financial inclusion for all groups of society.

Unsurprisingly in view of its commitment to customers, the bank has been the recipient of numerous international awards, having been judged ‘Best Islamic Bank in Jordan’ and ‘Best Islamic Finance Institution’ for many years by various international publications and institutions. The Levant region has a long and proud history of banking to which Jordan Islamic Bank hopes to continue contributing to for many years to come.

Over the past 30 years, Postbank has proven to be a stable, reliable and preferred partner. With the sum of this experience, we continue to overcome challenges of a varying nature, particularly in recent years. We invest in innovation, technology and a green future in line with our ESG strategy, because they make a difference in our sector.

The products and services we offer to our customers are developed in line with the contemporary market needs. The consumer experience is an immutable focus of the bank’s corporate policy. In addition, our leading goal is to be useful to our customers to the maximum extent by providing an outstanding experience and by offering modern solutions, spaces and concepts that best satisfy their needs at any place and time.