Sometimes, it can feel like the aims of the contemporary feminist movement are unduly focused in the cultural realm. While it is undoubtedly important for women to point out where other women are being unfairly depicted in movies, and where newspaper columnists are still furthering outdated stereotypes, there are also a number of more direct steps that can be taken to provide women with financial security, safety and justice.

That appears to be the current view of the UN Capital Development Fund (UNCDF), at least, which on International Women’s Day took the opportunity to outline their approach to promoting financial inclusion and equality for women around the world. The panel discussion that followed their statement was both lively and informative and revealed much about the international agency’s approach to financial inclusion. With a new generation of leaders emerging, what do these different approaches to promoting financial inclusion mean for the future of the feminist movement?

Support network

If the UNCDF’s approach to financial empowerment can be summed up in one word, it would be agency. Instead of providing women around the world with direct support, the organisation is largely focused on encouraging governments and corporations, providing them with the tools they need to help themselves. Their work, in other words, is always mediated by national and economic factors.

In some ways, this approach could be criticised for being too indirect. However, as an autonomous organisation with limited ability to make or enforce rules or economic mechanisms, it is somewhat inevitable that even the emerging generation of UN leaders see their mission in this way. And in fact, taking this indirect approach could be more beneficial in the long term.

Or, at least, that is the view of recent reports on promoting financial equality. According to a recent Women and Money report: “Money is the domain of men. Society doesn’t view it as a woman’s role to earn money, or her right to make financial decisions.” This anecdotal claim is also supported by hard numbers. Statistics from the United Nations show that there is a serious digital gap between men and women. For example, women are 35 percent less likely to have access to online services and 12 percent less likely to own a phone than men.

According to the UNCDF, this divide is largely the result of ‘gatekeepers’ barring women from free and equitable access to economic resources. They point out that there are 115 countries where the laws currently do not allow a woman to run her business in the same manner as a man can run his. Equally as concerning, the same report found that there are over 167 nations that have at least one regulation or law that severely restricts economic opportunity for women as well. Further, in many cultures, fathers, brothers, or husbands control finances on behalf of women. In this context, it’s becoming increasingly apparent that gender blindness is not a measure of workplace equality. Rather, instead of treating men and women as though they have the same level of economic agency, we need to actively support women who have been barred from it.

Promoting awareness

Granting increased financial and economic agency to women around the world will require a number of distinct strategies. One of these – and one of the most important for the team at the UNCDF – is simply pointing out that there is a problem (see Fig 1). That might sound obvious, but in many places around the world it can be difficult to challenge entrenched gender stereotypes, even for powerful international organisations like the UNCDF. Often it must work through indirect means in order to avoid directly challenging an entrenched – and often predominantly male – hierarchy.

As such, the organisations’ primary mechanism of action for much of the past decade has been to launch educational programmes for women in developing nations. One of the most recent of these, called the ‘Sprint4Women’ competition, allowed different digital finance providers to test out their business models in the field.

These models were then pitched to judges for formal review. Though the outcome of such programmes seems tiny in comparison to the scale of the problem – at first glance, little more than the launch of a new fintech brand – the UNCDF hopes that it will have knock-on effects on the role and power of women around the world. Indeed, they say, one of the reasons why countries have had such varying success in empowering women to take control of their own finances has been because some have overlooked the inherent link between education and empowerment.

Safety and security

Alongside the kind of educational programmes the organisation has been convening for more than a decade, the UNCDF is also keen to recognise the value and potential of technology when it comes to promoting financial inclusion for women. The rise of app-based banking and finance might lead to a huge shift in the way that women access and manage their financial lives. If, as the UNCDF points out, many women are barred from greater financial freedom by male gatekeepers, it might be possible for them to circumvent these obstacles by using contemporary technologies to directly access financial support.

There are 115 countries where the laws currently do not allow a woman to run her business in the same manner as a man can run his

There are risks involved with this approach, however. Though banks are shaking up the status quo when it comes to accessing finances, they are still reliant on a fairly outdated model of security. Financial fraud is still a huge problem around the world, and women are more likely to be victims of it than their male counterparts. Arguably tighter security measures are needed for comprehensive money management via smartphone apps. Instead, it may be preferable to allow women in developing countries to contribute to the development of financial mechanisms and technologies.

Only by including women at the macro-economic level are we likely to be able to make a real change in their lives. While such a focus runs counter, in some ways, to the UNCDF’s focus on empowering individual women, it may eventually be unavoidable if we are to realise actual change.

The bottom line

Ultimately, the focus on the emerging generation of UNCDF leaders is actually quite a ‘retro’ one. For much of the past 50 years and with the historical impact of the cold war, organisations like the UNCDF have been somewhat trapped by the ideological requirements of their backers. In the 1960s, for instance, it was difficult to point out the direct link between economic and cultural empowerment, because such an argument also lies at the heart of Marxist thought.

Now, it seems that a new generation has more freedom to express their views, and is less tied to the politics that inform them. They are able to simultaneously recognise the importance of corporate diversity and government-backed inclusion programmes. And this pragmatism might, in the end, be the most effective tool we have for empowering women around the world.

A relative upstart in the industry, the 17-year-old low-cost carrier opted to push on with an expansion plan while closely watching the pennies. First though, the team led by founder and chief executive József Váradi moved fast to take remedial action. “Wizz Air gave probably the most agile response to the pandemic-related loss of travel possibilities,” he told World Finance. These instant measures included the introduction of a strict hygiene code to keep customers and crew safe. In a confusing regulatory environment, an online travel map was developed so that passengers could keep up to date with official restrictions. And although Wizz Air had little experience in the freight business, it quickly built up a cargo operation to defray losses.

As some European airlines struggled for survival, bleeding billions, management conscientiously managed the bottom line. “Wizz Air continued to focus on strengthening market position and protecting liquidity during the third quarter of 2020 as sustained government restrictions severely obstructed air travel,” Váradi told shareholders in a briefing on performance. Every flight had to pay its way as best it could, or at least not lose too much. “We have a relentless discipline on cost and cash management while maximising cash returns on the flights we operate,” explains Váradi.

The result is that Wizz Air was able to boost per-passenger revenues under the vital measure of available seat kilometres (ASK), despite much lower loads. It was a classic lesson in management for turbulent times. “Wizz Air has ended up the biggest airline in Europe during the summer season with comparatively high load factors,” Váradi continued. “The airline managed to remain a resilient business while most of our peers suffered immediate financial issues.” It certainly helped that Váradi has a master’s degree in economics.

Unstoppable growth

Just before the pandemic hit, Wizz Air was on a seemingly unstoppable growth path. Within a decade of its first flight in 2004 – a hop from Katowice to London Luton – the airline had become the largest low-cost carrier in Central and Eastern Europe. In 2015, it was listed on the London Stock Exchange. In 2019, the airline’s 15th birthday, it carried its 200-millionth passenger and in 2020, Wizz Air was the first ever ultra-low cost carrier to be named ‘airline of the year’ by Air Transport World.

The airline was one of the few to provide customers with cash refunds and is emerging relatively unscathed from the chaos. Although ticket revenues in the third quarter collapsed by nearly 80 percent and ancillary revenues by 73 percent, leading inevitably to losses of over €114m, Wizz Air still retains €1.2bn in cash.

As other airlines shrank their operations as fast as they could, Wizz Air persevered with the development of new bases in Oslo, Bari, Catania, Palermo, Milan Malpensa, Rome, Sarajevo, Bourgas, Dortmund, Tirana, Lviv, St. Petersburg, Bacau, Larnaca, Doncaster Sheffield, London Gatwick and Cardiff while doubling the size of its base in Abu Dhabi to four aircraft.

And in a real coup, Wizz Air Abu Dhabi staged its inaugural flight to Athens on January 15, opening up a swathe of new routes. “Despite a distorted playing field, the performance of the new operating bases is in line with expectations,” reports Váradi. “Unlike other airlines, we have remained ambitious and continued to expand our geographical presence over the last year.”

As normality slowly returns, Wizz Air finds itself in a good position as it boosts liquidity simultaneously with tightening its belt. In January 2021 it successfully floated a €500m three-year bond issue on favourable terms that reflects a highly desirable investment-grade credit rating. “Wizz Air is even better positioned to deal with the uncertainties associated with COVID-19,” said the chief executive. “At a rate of 1.35 percent, the bond was issued significantly below the interest costs of competitor airlines.”

Looking ahead, Váradi is broadly optimistic. Feet firmly on the ground, he predicts that 2021 “will be a transition year out of the COVID-19 crisis” and that Wizz Air “will emerge as a structural winner” as passengers return. Wizz Air heads into the rest of 2021 with an updated, environmentally virtuous fleet.

The airline boasts 140 aircraft (see Fig 1) with an average age of 5.4 years, boosted by the addition late last year of five lean-burning Pratt & Whitney-powered Airbus Neos. With a highly flexible network in terms of regions, airports and countries, a robust balance sheet and travel-hungry passengers, Wizz Air is ready to fly. “Looking ahead, only the sky is our limit,” says Váradi.

Since Nigeria returned to democratic rule in 1999, the Republic has enjoyed enormous progress on account of democratic governance to varying degrees across all tiers of government. In Akwa Ibom State, it has been an admixture of accomplishments and a trailblazing catalogue of milestones in social, economic and political domains. This has made the State a genuine reference for the efficacy of experienced and focused leadership as well as a compelling destination for local and international investors and tourists.

Located in the coastal southern part of the Nigerian federation, Akwa Ibom has a GDP of $11.1bn, which is equal to the GDPs of Rwanda and Seychelles combined, and sits in the comity of Niger Republic, Benin Republic, Equatorial Guinea and several other African nation-states on the GDP index. Akwa Ibom’s historical, geographical, artistic, culinary, ethnographic and archaeological peculiarities make it an indisputably choice destination for business, leisure, cultural, faith and eco tourism. Lately, it has also been a destination for incentive and special interest tourism.

“With nature’s generous endowment, visionary leadership and a repository of smart-working people, Akwa Ibom has all the preconditions to blossom into a self-reliant, self-sufficient and self-sustaining state. The masterful collaboration of these factors is what has evolved the State into a prime destination for an assortment of people, businesses and interests,” Udom Gabriel Emmanuel, governor of Akwa Ibom, told World Finance.

A 2019 McKinsey Report titled ‘Nigeria at a crossroads; getting Nigeria where it belongs’ stated that emerging economies “that have been able to generate growth and raise prosperity, through poverty alleviation and the emergence of a new wave of middle and affluent classes” are regarded as outperformers. The outperforming benchmark touted by McKinsey was reached and surpassed in Akwa Ibom stimulated by tailwinds instigated by an enterprise outlook to administration and governance.

Until Udom Emmanuel assumed office as governor in 2015, the ‘civil-service state’ epithet was the State’s bane. The unfortunate narrative imposed an impropriety that leaned on a flawed understanding of the intricacies at play, and disparaged the myriad implications and losses from such progress-inhibiting dogma.

Compelling desire

From the outset, the mission was founded and still revolves around a compelling desire to transition Akwa Ibom into an inclusive enterprise State, through leveraging enormous material and qualitative human resource endowments to make the State an irresistible component across several value chains and productive partnerships that take into account the country’s inputs, advantages and idiosyncrasies.

Subsequently, the administration adopted a progressive pathway because of its strategic importance in giving orientation and focus to the growth and sustained advancement of the local economy. As a result, upending the appetite for either tagging along or playing catch-up in such a rapidly changing world is a cardinal policy imperative of the Akwa Ibom government. According to Udom, this is based on the realisation that “genuine progress is a function of our collective divergences, our shared identity, common priorities, and values that transcend our differences, amplify our uniqueness and enable us to build workable relationships and partnerships that align effectively and efficiently for all Akwabomites.”

The resolve to transition Akwa Ibom to an enterprise State was captured in a blueprint that offered an amenable roadmap for achieving renaissance along the routes of job creation, wealth creation, poverty alleviation, infrastructural consolidation and expansion and ecopolitical inclusion. Subsequently, upon assumption of office, Udom set up a remodelling committee to engender a social contract and a technical committee on foreign direct investments (FDI) to promote, midwife and enhance the flow of investments into Akwa Ibom.

The result is a horde of firms including the largest syringe manufacturing factory in Africa, an electrical-digital metering solutions manufacturing factory, rice mills, palm oil processing plants and flour mills to mention a few. Added to the volley of strategic partnerships is the emergence of hundreds of businesses and thousands of jobs that, with ripple and multiplier effects, phenomenally impact the livelihoods of Akwabomites and Nigerians.

With a business-inclined disposition and private-sector approach to governance, the governor began by aligning the measure of progress with economic indices and other relevant economic indicators, thereby thrusting his administration on an economic pivot largely bereft of the customary politically dictated metric. “As a first step, rather than establish a political fortress, I opted to build an economic infrastructure that bequeathed socio-economic power and ultimately political inclusion across all strata of the State. The intention was to engender a strong economy that would generate income, elicit productive partnerships, and create opportunities for local and foreign investments into Akwa Ibom,” Udom said.

As a direct outcome of the resulting paradigm shift, governance was re-engineered towards an enterprise orientation model away from the traditional receipt and distribution approach that sustains futile expending and stifles the strategic attitude towards stimulating and managing the smart administration of resources.

Udom and his team leveraged the State’s comparative advantages, the varying signature strengths of its people, to deconstruct and reinvent the approaches to citizenship and doing business in Akwa Ibom. To this end, the government created sets of possibilities for value chain creation in the areas of public sector job enhancement, private sector orientation, sociopolitical inclusiveness, sustainable infrastructure development, and entrepreneurship across sectors including the hospitality, creative, logistics and tourism industries. To propel and sustain the various outcomes therefrom, the State underlaid its unique and intrinsic advantages of excellent people, a peaceful environment and a supportive tradition at the base of all endeavours and engagements across the private and public sectors.

Creating sustainability

Earlier, there were talks about the dreadful implication of almost exclusively relying on a single source receipt status, to develop and make the State sustainable. The governor recalibrated his administration by transitioning the State into a business conglomerate. With thoughts enunciated in declarations like “horticulture must be supported to make a huge contribution to our GDP, logistics is an essential key to the future, knowledge and data are the new oil and our greatest asset is our people,” it was clear that he had his eyes on evolving a State with an enterprise-orientation.

Subsequent to this, Udom and his team chose an industrial policy pathway to deliver on the vision. They opted for that because of its big push approach and its strategic significance in giving gumption to the focus on the growth of the local economy by upending the appetite for exogenously induced growth in favour of internalising productive and positive externalities; a situation akin to import substitution and export promotion strategy.

According to the governor, the State requires development that is created beyond the precinct of subsistence agriculture and statutory allocation. He opined that while horticulture accounts for a great part of employment in the State, with strategic decoupling and increased productivity, its capacity to absorb more members of the population along the various value chains of the sector, from cultivation through processing to packaging are added elixir to the flurry of micro, small and medium enterprises.

An excellent aspect of the State’s industrial policy pathway is the awareness of the possibility of capsuling, which the administration reckons will happen regardless of an industrial policy. To this end, the Udom administration verbalised and practicalised protection and enablement via regulation and monitoring for firms in a manner that espouses genuine interest, unflinching commitment, partnership and collaboration. This is a classic instance of government facilitation with a visible impact on disabling bottlenecks at the infrastructural, policy and regulatory levels.

According to the governor, another aspect of the policy is the “responsive and cooperative ecosystem in the State partly represented by the supportive disposition of the people, peace and security in the State, the visible reduction in transaction costs through enhanced infrastructure and the annihilation of virtually all illegitimate taxes in a further bid to mitigate capsuling and freeing sources and resources.”

Evidently, the uniqueness of the investment environment of this enterprise State is that it also allows for the evolution of capsuling in some very capital-intensive industries that have either comparative advantage, absolute advantage or technological advantage. “This is principally to encourage FDI in some select sectors because in the administration’s understanding, if such flexibilities to secure and develop such sectors are not enthroned and monitored, capital and investments may not feel safe, and as a result, the rent-seeking activity would be inadvertently encouraged,” Udom said.

The inflection point

The ability to connect more deeply at all levels, to sense and stimulate reactions and desired interactions is at the heart of the purpose of the people and the State. In Akwa Ibom it is self-evident that progress is a function of unanimity of purpose, inclusion, harnessing extant diversities as much as it is a culture of shared identity, prioritisation and value enthronement. These values transcend variances, amplify uniqueness and enable the creation of sustainable relationships and partnerships that work together effectively and efficiently in the interest of the State and its citizens.

Udom’s excellent sense of judgement and business integrity was earned from long-term meritorious and untainted service in the corporate world, in which he was among the defining figures. His ambidexterity, as exemplified in the way he balanced autonomy and dependency, and his intrapreneurship fervour, are part of the vast capital and collateral that have helped investors’ confidence.

Rather than establish a political fortress, I opted to build an economic infrastructure that bequeathed socio-economic power

The resulting structure ushered in a feeling of ownership, a sense of urgency, of team spirit and established positive momentum as well as enthroning a supportive culture, all of which blended to checkmate prebendalism, lethargy and malfeasance in public service delivery. Just two years into the administration of governor Udom, the benefits of his enterprise approach to governance were evident. The Q3 report of the Nigerian Bureau of Statistics (NBS), the country’s apex institution for socioeconomic and development statistics, declared Akwa Ibom the second-best state for attracting FDI into Nigeria.

The PPP model

In Akwa Ibom, the functionality of the public private partnerships (PPP) model is palpable. The allure of PPP, which is hugely dependent on the predictability and steadiness of the socioeconomic and political environments of any ecosystem, finds comfort in the State, which is thought to be the most peaceful and accommodating State in Nigeria. The PPP model berthed a steady transformation of the local economy in a way that prioritised value creation, value addition and wealth creation as well as waste management in the context of enterprise orientation. The resultant enterprise State made for a shift to a culture of diversifying the State’s revenue portfolio and in the process bestowing alternative strategies that engendered economic activities that are revenue-generating and that create veritable grounds for taxation. The thoughtful establishment of a structure that nurtures the social, political, economic and institutional actions vital to precipitating the socioeconomic, ecological, and cultural wellbeing of business, governance and non-aligned interests, confirm the emergence of Akwa Ibom as an enterprise State.

Added to this is the secure and peaceful nature of the State. By the admission of the Nigeria Police, Akwa Ibom ranks as the State with the lowest crime index in Nigeria, as was affirmed by the Nigerian Army under the auspices of the General Officer Commanding the 6 Division who described the State as the “safest in Nigeria.”

All types of preneurs

In Akwa Ibom, it is commonplace to hear words like, ‘agripreneurs,’ ‘youthpreneurs’ and ‘ICTpreneurs,’ which are suggestive of the enterprise approach of the administration towards public sector governance, private-public-sector collaboration and economic management.

Regarding ‘youthpreneurs,’ Udom said that preparing young people for socioeconomic leadership through a systematic onboarding process is a manifest imperative. “We believe youths are the most dynamic asset of our community and this is evident around the world where youths have been credited for taking some countries to near double-digit growth as net contributors to the economy. Worthy of mention is the Nigerian Entertainment goldmine, which is worth about $10.5bn for which as an administration we are determined to encourage and support our youths to unleash their entrepreneurial and creative talents to tap into.”

In regard to ‘ICTpreneurs,’ Udom said that the main preoccupation of his administration is to create conditions that favour organisations and private individuals to innovate and create. “To this end, we have a focus on attracting investments to nurture talents in the digital industry where our vision is two-fold, consisting of investing in developing skills in areas including coding, application development, embedded programming and data analytics, and afterwards supporting the generation of ideas, and eventually wealth, by creating a hub for digital contents that would include production of digital solutions, animations and new media solutions.”

Preparing young people for socioeconomic leadership through a systematic onboarding process is a manifest imperative

These industries have grown exponentially in the last year, going from revenues of $23.1bn to $115bn and projected to continue growing.

Similarly, the initiative of ‘agripreneurs’ is targeted at farmers in the State to avail the benefits from new ideas, alliances and available incentives. “In this light, we are introducing an integrated agriculture and aquaculture model in addition to building platforms to scale up their engagements and facilitate selling their produce statewide and nationally. The focus here is on ensuring ample food supply, processing, storage and distribution and, equally important, wealth for the farmers,” Udom said.

A common thread that runs across all the ideas and initiatives is the wire and wave of knowledge and technology to make governance easy, accessible, cost-effective and process effective.

There is also ingrained in the system the need to create an ecosystem for fundamental innovation because of its enormous potential to bridge the disparities between socioeconomic groups. Udom elaborated: “I reckon that no object in nature is completely autonomous, and when this realisation of interdependence is applied deliberately and decisively, unity becomes an inevitable output. The kind of output that draws from the uniqueness of individuals and diversities of societies in a collaborative fashion. To this end, to unite with understanding by tolerating and accepting to work together in recognition of the uniqueness of others, and an appreciation of what they contribute to the common interest is non-negotiable.”

The Dakkada Tower

Inclusive politics

The major drivers of the State’s development revolve around supporting inclusive politics, based on transparent and predictable mechanisms that include and engage individuals or social groupings commonly marginalised or wholly excluded from political life as well as fostering resilient societies, chiefly by promoting robust state–society and society–society relations.

In the medical sector, the realisation that progress was limited by a fragmented and disoriented medicare system bereft of a reasonable understanding of the complexities of public healthcare and developments in the modern health care infrastructure and administration were addressed head on. Subsequently, the State struck a healthy balance between world-class technologically enabled medical facilities and best-in-class trained medical personnel to make the sub-sector one of the best in the entire West African sub-region. The intention was foremost to ensure that the medical needs of Akwabomites are met, graduating towards enhancing the facilities and personnel to the extent that Akwa Ibom becomes a destination for medical tourism.

Similarly, the State’s educational infrastructure has been restructured and realigned in favour of developing skills, proficiencies and abilities required across different job types and work settings to address present and future needs of the State and the businesses within its domain. This is based on the knowledge of the changing workplace and an appreciation of the declining influence of oil and gas. This is in addition to encouraging an entrepreneurial mindset for Akwa Ibom citizens, hopefully forging creators of employment opportunities instead of just potential employees.

The State sought and consummated partnerships especially within the private sector with the intent to create and develop sustainable synergies. For instance, the State partnered with all the oil giants operating within its domain and fulfilled part of its commitment by erecting a 20-storey state-of-the-art building to accommodate the oil firms and related institutions to enable the effectiveness and efficiency of their operations. This is complemented by the micro, small and medium scale enterprises framework, which is aligned around sectors that are either directly or indirectly related to services and offerings of these oil sector actors.

It is to the credit of the Udom-led administration that Akwa Ibom is no longer landlocked with the construction of over 2,000km of economic roads, no longer waterlocked with the ongoing work on the Ibom deep seaport project (IDSP) and certainly not airlocked to local air travel. With work nearing completion on the international airport service, the State is indeed emerging into a far-reaching hub in Nigeria and Africa.

All of these projects, in addition to the huge network of economic roads spread strategically around the State, have indeed opened up Akwa Ibom to investor and tourist traffic either by road, water or air and this is poised to elasticise with multiplier effects across markets, sectors and livelihoods.

Akwa Ibom International Stadium

Major socioeconomic drivers of the state

Complimented by other factors, the model in place in this enterprise State has resulted in a steady transformation of the ecosystem in a manner that prioritises wealth creation, value addition and inclusiveness within the framework of enterprise orientation. And in the words of the chief visioner, “this is one of our deliberate shifts in favour of a system that fuels the requisite social and economic advancements required to foster the participation and well-being of communities as a condition to evolving Akwa Ibom into an inclusive enterprise State,” Udom said.

Akwa Ibom is on its way to achieving absolute advantage in certain spheres from which there will be a lasting legacy

The resulting structure, its accompanying processes and approaches, combine deep insight into the dynamics of governance and administration with collaborations that ensure that through institutionalisation, Akwa Ibom is on its way to achieving absolute advantage in certain spheres, from which there will be a lasting legacy. There are other unrelated but enormously impacting activities in the state for which the governor said, “as a complement to other economic activities in the state, we are deliberate on evolving ‘agripreneurs,’ ‘youthpreneurs,’ ‘ICTpreneurs’ and ‘womenpreneurs’ as major drivers of the State’s overall development trajectory.” There is in place an evolving system that prepares citizens, especially young persons, irrespective of sex and gender, to meet and surmount challenges and achieve their dreams. In the governor’s words, “we are achieving through supporting inclusiveness based on transparent and predictable mechanisms, value creation protocols and by fostering resilient state–to-society and society–to-society relationships, as a first step. Escalating very productive relationships becomes a natural course of action.”

This is promoted through initiatives, involvements and engagements that accentuate social, ethical, emotional, physical and cognitive competencies in a manner that progresses their skills and prepares them for positive and productive impacts, for the short, medium and long term.

“In Akwa Ibom, it is self-evident that none of us is as impacting as all of us and this is from our understanding that in working together for the common good, we benefit Akwa Ibom State, Nigeria, mankind and by extension, ourselves. Herein lies the Akwa Ibomites Faith of Greatness enunciated in our creed,” Governor Udom concluded.

Since 2002, Access Bank has fully transformed from the lesser-known institution it was, then ranked 65th among 89 banks operating in the country, into a world-class African financial institution. Today, it is one of the three largest banks in Nigeria (in terms of assets, loans, deposits and branch networks), leading the way in at least three of these categories. This feat is due to a robust, long-term approach to client solutions.

Access Bank has leveraged its strength and success in the corporate, personal and business banking platforms after the acquisition of Nigeria’s Intercontinental Bank in 2012 and Diamond Bank in 2019. As part of its growth strategy, Access Bank focuses on mainstreaming sustainable business practices into its operations and strives to deliver sustainable economic growth that is profitable, environmentally responsible, and socially relevant. Through Access Bank, some of the biggest companies in Africa across construction, telecommunications, energy, oil, and gas sectors have recorded significant progress.

To take advantage of the African Continental Free Trade Area agreement (AfCFTA), Access Bank plans to establish its presence in 22 African countries. This will also enable the bank to diversify its earnings and take advantage of growth opportunities in Africa. The string of expansion efforts has commenced across Africa, including Cameroon (operating licence), Kenya (Transnational Bank), Zambia (Cavmont Bank), Botswana (BancABC Botswana), and most recently, South Africa (Grobank Limited).

Banks play a role in transforming their local and regional economies, ultimately making them inclusive, green, digital and sustainable

World Finance spoke to Herbert Wigwe, the CEO at Access Bank, “Our strategic actions in the past 12 months evidenced a strong focus on retail banking and financial inclusion, an African expansion strategy and a drive for scale and its economic benefits. We know there is a significant gap in achieving our vision to be the world’s most respected African bank. As such, we are very focused on closing this gap through strategic and disciplined expansion of our African footprint, leveraging robust technology platforms and exceptional customer service delivery.”

“Our geographical diversity is a core element of our business model, providing opportunities for growth in different economies and enhancing resilience. We have acquired the exceptional capacity to successfully execute mergers and acquisitions with speed and efficiency at minimal risk while delivering value to shareholders. The series of mergers and acquisitions we have undertaken since 2005 all bear testimony to this and have all been value accretive,” Wigwe said.

Global payment gateway

Africa has enormous potential with increased opportunities for an African bank such as Access Bank, which is well run, understands compliance, supports trade and has the appropriate technological infrastructure to support payments and remittances without taking incremental risks. The bank focuses on serving as an aggregator in Africa to build a global payment gateway, provide trade finance support and correspondent banking in key markets across the continent.

The retail franchise has also grown over time, contributing almost double to the franchise in four years on the back of a strong focus on consumer lending, payments, remittance, customer acquisition, and digitisation. This is demonstrated in the bank’s position as the largest issuer of Visa cards in Africa and the largest disburser of consumer loans in Nigeria. Access Bank’s retail banking aspiration is for one in every two Nigerians to bank with them by 2022. In 2020, it ranked number one in retail banking income in Nigeria with over N56.1bn ($136m) in fee income from its digital banking platforms and alternative channels. This performance is in keeping with its aspiration to be the number one retail bank by customer base and revenue.

Access Bank recently disclosed a plan to transition into a holding company (HoldCo) structure and has received the ‘approval-in-principle’ from the Central Bank of Nigeria for the restructuring. The HoldCo will consist of subsidiaries in the consumer lending market, the electronic payments industry, and the retail insurance market.

Upon completion of this process, the Access Bank Group will consist of African and international subsidiaries, while the payments subsidiary will leverage the assets of Access Bank. The resilience of Access Bank is reflected in its exceptional growth over the years. This is particularly evident in the bank’s financial performance in 2020 with significant increases in revenue and profitability, despite the challenges posed by the economic crisis triggered by the COVID-19 pandemic.

In the past decade, the bank has grown tremendously not only in its financial performance, but also in its social and environmental prowess. The effectiveness of the bank’s strategy to be the world’s most respected African bank, and indeed, Africa’s gateway to the world, is deeply rooted in its commitment to sustainability.

Sustainability credibility

In 2020, Access Bank continued to lead numerous efforts that propel both its sustainability targets and its African gateway strategic drive. The bank was granted a sustainability certification by the European Organisation for Sustainable Development (EOSD), under its Sustainability Standards and Certification Initiative (SSCI), on September 30, 2020, at the World Development Finance Forum (WDDF) in Karlsruhe.

It came as no surprise that Access Bank was the first commercial bank in Africa to achieve this. This certification is a reaffirmation of strong sustainability leadership and it is worth noting that only globally reputable financial institutions are pre-qualified for the SSCI certification program, and they are required to have a demonstrable commitment to sustainability. Access Bank signed up to SSCI in July 2018 as one of the carefully selected financial institutions to pioneer the implementation of the standards.

The institutions involved in the co-creation of the standards represented a broad spectrum of stakeholders in the financial services industry. Over the next 18 months from July 2018, the council met regularly to review the draft sustainability standards, and watch presentations from the applicant financial institutions about their implementation milestones and challenges, and provide feedback.

There are core principles that underpin these sustainability standards. The standards help banks play a role in transforming their local and regional economies, ultimately making them inclusive, green, digital and sustainable. Furthermore, the banks are to pursue profit alongside social responsibility and environmental protection.

The EOSD was also very useful in providing technical guidance to the banks between the in-person meetings before the pandemic hit in Q1 2020. Access Bank was also appointed as a member of the International Council for SSCI and contributed to the all-encompassing framework for holistic sustainability integration, the broad purpose of which is to drive innovation in the organisational culture of financial institutions.

In a congratulatory message, the EOSD affirmed that Access Bank “fulfilled the criteria of the first-ever holistic, robust, and locally-sensitive set of standards to make value-driven financial institutions more resilient and profitable. Financial institutions play crucial roles in implementing national development plans, the UN Sustainable Development Goals and protecting the natural environment in which they operate.”

Wigwe commented on the certification, saying, “Access Bank’s sustainability approach is driven by a desire to impact lives positively now and in the future. We are committed to ensuring community wellbeing and prosperity while fostering sustainable economies across Africa.”

Guiding role

Presenting to the diverse audience attending the WDFF before the ceremony for the SSCI certification, Omobolanle Victor-Laniyan, Access Bank’s Head of Sustainability, provided the highlights of the sustainability journey of Access Bank. This included the launch of the Access Bank sustainability strategy 13 years ago and its guiding role in creating the Nigerian Sustainable Banking Principles (NSBP), now a regulatory instrument of the Central Bank of Nigeria (CBN).

Access Bank is also an early adopter or co-creator of many international initiatives for sustainable banking, including the Equator Principles, GRI reporting, UN Global Compact, UN Principles for Responsible Investment, and UN Principles for Responsible Banking. The commitment and performance of Access Bank on sustainability have been reaffirmed unquestionably by its receipt of the Central Bank of Nigeria’s Most Sustainable Bank of the Year Award three years in a row since its inaugural edition in 2017.

Now, more than ever before, global finance inexorably steers towards sustainable finance. The SSCI is a practical tool for transforming banks in terms of organisational purpose and setting measurable high impact goals, which drive institutional governance, culture, and business models. It assists the support of institutional sustainability despite the constant evolution of the financial ecosystem. The Nigerian banking industry sees financial technology firms competing with the incumbent, traditional banks. Hence, all banks must embrace holistic sustainability to thrive in the current climate by renewing their social licence to operate and consider the overall wellbeing of the planet.

As a sustainability-certified organisation under the SSCI programme, Access Bank can uncover and harness new income streams and thrive for the long term in an ever-changing world. Access Bank pledges that it will continue to significantly manage its footprint and propel its customers and stakeholders towards a more sustainable path aligned with the UN Sustainable Development Goals (SDGs) and other global sustainability standards.

Environmental, social and governance (ESG) issues have gained space on the financial market’s agenda. Companies around the world have been reviewing their business models to integrate ESG commitments that go beyond the traditional agenda centred exclusively on shareholder value creation. The value of a company is now viewed on a broader approach – what the company brings to employees, clients, suppliers, investors, governments and to the society as a whole. The name of the game is the admirable profit – harmonising financial results with impact on the society and contribution to future generations.

That is not a new concept, and the acronym is widely known in the market. But why are we only now seeing it everywhere? It all started in Europe as a result of the actions of NGOs and think tanks related to these issues, and then it went to the individuals. Those individuals are also investors, and started to demand that money managers incorporate the broader approach to the investment decisions those make on their behalf.

Times have changed for good and for the benefit of the global society

The pandemic collaborated to expedite the process, given the growing concern about protecting people and the environment. Moreover, ESG aspects also started to be seen as risk factors. How well a company deals with those aspects may determine how economically sustainable the business is going to be in the future. That has a deep impact on valuations and on the analysis by fixed income investors of a company’s capacity to generate cash in the future to repay its debt obligations.

Meanwhile, consumer trends are also changing dramatically, for many reasons that include generational aspects. According to a study by Morgan Stanley, 86 percent of millennials are interested in sustainable investments, and those same individuals are also consumers.

According to a report by BoFA & McKinsey, it is estimated that 60 percent of millennials consume brands with strong social and environmental responsibility. We are dealing with a public that debates consumerism, condemns environmental degradation and increasingly fights for social justice. It is all related and integrated.

Good for the world

At Suzano, the world’s leading pulp producer, one of our cultural drivers states that ‘it’s only good for us if it’s good for the world.’ This concept is present in all our initiatives and determines how we practise ESG on a daily basis. We see the growing importance of ESG not only as the right thing to do, but also as a huge business opportunity for a company on the right side of the history, renewable raw materials, biodegradable and recyclable products are part of the solution.

The phenomenon is also present in financing activities. Last year we decided to launch our sustainability-linked bonds (SLBs) and became the second company in the world to go for that structure. The SLBs are debt instruments with the interest rate linked to the achievement of sustainability targets. We issued a total of $1.25bn, priced at Brazil’s lowest interest rate ever for a 10-year issue.

This means that, for the first time ever, investors were willing to accept lower interest rates for an instrument that potentially creates positive externalities (ESG goals). Today, 30 percent of Suzano’s debt is linked to ESG features (SLBs, sustainability linked loans, green bonds). In other words, there is a vast market to be explored, and the demand for these instruments represents one of the potential ways to monetise a robust ESG strategy.

Times have changed for good and for the benefit of the global society. Every company may have a role in that process that is bigger than the achievement of financial results. It is up to every one of us business leaders to find our own way to contribute.

Turning 30 feels, to many, like the start of something new. It is a moment to embrace a more mature outlook, to consider the past while looking to the future. This holds true for institutions, just as it does for individuals – or at least that’s the case for Bulgarian institution Postbank, this year celebrating three decades since it was founded.

It’s been a tumultuous 18 months, but Postbank has navigated the challenges of the pandemic thanks to its flexibility, commitment to personalised service and willingness to learn. Drawing on its 30 years in the international banking space, the institution is now looking to the next 30.

World Finance spoke to Petia Dimitrova, CEO and chairperson of the bank’s management board, about embracing digitalisation and supporting Bulgarian entrepreneurship going forwards.

In 2021, Postbank celebrated its 30th anniversary. How would you describe the past year?

In 30 years, Postbank has proven itself as one of the most successful banks in Bulgaria, an excellent partner, employer and socially responsible company. We have solidified our position as an institution that customers trust, having spent the last three decades opening up a universe of new opportunities to them.

Thanks to this shared trust we are third in terms of loan portfolio and the fourth largest bank in Bulgaria in terms of assets and deposits, with a market share of over 10 percent. We boast more than 200 branches nationwide and, over the last five years, we have received over 100 awards for our digital innovations and products, as well as for our services and social responsibility policy.

These digital solutions are extremely intuitive, making banking easy, pleasant and fast

The pandemic once again shows us that whatever plans we may make for the future we can never foresee what will happen in reality. Life does not stop – customers need immediate solutions, not ones that take weeks or months. Preparation is essential – we’ve learned that we need to have tailored solutions at the ready so that customers feel they are benefiting from a personal approach.

There is no doubt that now, a year and a half later, trust in the Bulgarian banking system is greater than ever before. All the indications point to the fact that, despite the difficulties we face together, the banking system is and will be an important factor in the post-crisis recovery period. Recent months have shown us that change is possible – in terms of how and where we work, shop, communicate and rest. I hope we can continue to learn lessons from the many examples of positive change we have seen since the pandemic began.

The COVID-19 crisis stimulated digitalisation. What special products and services have you offered your customers during this period?

Excellent customer experience remains a priority. Consumers expect and require us to support their plans even faster and via the most convenient channel – the digital one.

Following the increased active use of digital channels by the bank’s customers, the total share of transactions carried out online on an annual basis reached 78 percent at the end of 2020 versus 22 percent carried out in a branch. The growing trend in developing the bank’s digital channels is also confirmed by annual usage data, with the m-Postbank mobile app seeing the most significant increase in use. Over the last year, the number of active users of the app grew by 60 percent and the total number of transactions carried out increased by 50 percent compared to 2019.

What trends do you observe in terms of customer requests?

Our clients want a personal approach – they want to have access to their money at any time and in any place, to receive a personally developed offer and to feel special. We strive to know our customers as well as possible and offer them personalised services and products based on their behaviour and preferences.

As digital payment services continue to grow, most providers will be focusing their efforts on instant payments. This is a huge challenge for us all and one we are ready to face thanks to an exciting innovation we recently introduced – our digital wallet. I am certain it will be a new, unique and impeccable experience for customers seeking the best solution for managing their personal finances.

Customers transfer the contents of their physical wallet, digitally, to their mobile phone. They have the opportunity to add all of their cards, and the wide range of functions provides instant active access to their funds, meaning that they can manage them 24/7. These digital solutions are extremely intuitive, making banking easy, pleasant and fast. You save not only time but also money, since the fees for digital transactions are lower.

One of the biggest investments and innovations we’ve launched at Postbank is our digital self-service zones. These are areas within our branches where customers can carry out most of our main banking transactions themselves without having to be registered for online banking.

They simply use a debit or credit card to identify themselves. Digital zones are already functioning in 41 branches across 20 cities nationwide and more locations and service upgrades are yet to be unveiled. Already they are recognised as a preferred alternative to other in-branch services.

What lies ahead for Postbank in 2021?

Other than innovative digital products and services, we at Postbank continue focusing our efforts and funds in supporting projects with real added value for society. We believe that one of the greatest benefits we can bring will be building awareness of the need to change life for the better.

For the third year in a row we are participating in the ‘dare to scale’ project – a four-month programme for growth aimed at entrepreneurs and businesses already past their initial development stage and currently focusing on their activities. The programme is organised by the Bulgarian office of the global entrepreneurial network, Endeavor, with Postbank as the main partner.

It is extremely important for us to be part of this process, to support the ambitions of companies seeking to scale up their business and thus change the entire ecosystem. The current moment presents an abundance of challenges but it will be to our benefit if they can help improve our sustainability and nurture our ability to learn and grow.

We at Postbank will share the power of our experience and expertise to support them at the most important stage of their business’s development. By engaging in partnerships like these, we embrace innovation and foster improved opportunities in the ecosystem as a whole. Investment in entrepreneurship is part of the change that keeps us moving forward.

Portugal has a long history of bringing the world closer together. The country’s global maritime exploration in the 15th century, mapping the coasts of Africa, Canada, Asia and Brazil, linked continents and cultures as never before. Five hundred years since early explorers set off across the Atlantic, diversity remains a central part of our welcoming culture and unique hospitality. In 2021, the world is closer than it has ever been – and, if the coronavirus pandemic has taught us anything, it is the viability of remote, global living. Portugal’s rich history has made it one of Europe’s top tourist destinations.

Our delicious food, amazing beaches, golf courses and enviable Mediterranean climate attracted almost 28 million visitors to Portugal in 2019 alone. Colourful, thriving cities such as Porto and Lisbon – one of the oldest capital cities in Europe, second only to Athens – complement the rolling green hills of the rural inland, and, of course, the paradise of golden sand and blue sea along our Atlantic coast. So, it’s no surprise that Portugal is home to the World Travel Awards’ best island destination (Madeira), city break destination (Lisbon) and beach destination (the Algarve). The Iberian Peninsula truly has it all.

Despite the pandemic, the Portuguese economy actually grew by around two percent in 2020. Currency stability, high returns on real estate and local investment funds, and the opportunity to diversify portfolios make Portugal a very attractive market for foreign investors. The country has a very affordable cost of living, thought to be almost 30 percent lower than the UK, and between five and 10 percent lower than Spain, and English is widely spoken – around 60 percent of the population is proficient – making for smooth international communication.

Portugal’s golden visa programme

The Portuguese residence permit programme, also known as the golden visa, is a scheme that grants investors access to Portuguese residency and citizenship. It is the only scheme that allows foreign investors to claim citizenship for themselves, and their families, without relocation: only 14 days every two years must be spent in Portugal. After five years, investors are eligible to apply for citizenship. Not only does the scheme provide good returns on investment, it also allows investors to secure the future of their families for generations to come.

The Portuguese passport consistently ranks among the most powerful and travel-friendly, granting visa-free access to more than 170 countries. As Portugal is part of the Schengen area, a Portuguese residence permit grants investors freedom of movement from day one, as well as the opportunity to start businesses in 25 other European countries.

In addition, investors when approved on the residency permit programme immediately gain the use of Portugal’s public hospitals at no charge, as well as access to European universities and job markets. Applying for a Portuguese golden visa brings a wealth of opportunity – from exciting business prospects to long-term plans for retirement and the education and career of the next generation – to high-net-worth individuals currently facing the obstacles that come with a weak passport or political instability in their home countries.

Portugal has one of the most accessible residence permit schemes in Europe. The Portuguese golden visa programme invites investors to claim citizenship in fewer years than comparable schemes in Spain (10 years) and Greece (seven years), and without relocation to Portugal. The Portuguese golden visa is fast, flexible – and affordable.

Investment options: real estate

The most popular golden visa investment option is real estate. A minimum investment of €280,000 can be put towards properties in remote areas that are over 30 years old and require refurbishment, some offering guaranteed rental income, though they may not provide high capital appreciation. Better returns on investment come from property in one of Portugal’s major cities, such as Lisbon or Porto, where 30-year-old properties in need of refurbishment require a minimum investment of €350,000 to qualify for the golden visa.

These properties are often well-located residential apartments, with the potential for tourist-targeted short rental periods. High demand for this type of property is driving up prices by as much as 10 percent a year. Investors committed to returns on investment are advised to put their money into new properties or off-plan projects in major cities, where capital appreciation can increase by up to 15 percent a year, and rental income can reach five percent a year. The minimum investment required in a property such as this is €500,000.

Investment funds route

However, investment funds are also becoming popular as a tax-efficient route that allows diversification of investment, and has been bringing returns of around five percent to seven percent a year. The minimum investment in qualified closed mutual funds is €350,000. This route is for those that normally prefer investing in funds, and are interested in having professional fund managers investing their money and diversifying their investment, in several different projects instead of just one property.

New golden visa investment options

Ninety-eight percent of applicants have been approved through either real estate or investment funds. The Portuguese golden visa programme has no grey areas.

As of January 2022, it will no longer be an option to invest in real estate in main cities and coastal areas for residential purposes. Residential property investment will only qualify investors for a golden visa in inland areas of mainland Portugal and the islands (€500,000 minimum, or €350,000 plus refurbishment). Investors interested in having a residential property around one of the main cities or desirable coastal areas should proceed as quickly as possible, as demand is high.

Getting started

PTGoldenVisa is an integrated service provider for foreign investors in Portugal, offering a credible, confidential end-to-end service informed by our expertise in law, economics and international commerce. Our focus on the Portuguese programme sets us apart from other golden visa firms – we are not a marketing department promoting numerous residency programmes, but a team who assist clients for the entire five years till they are granted citizenship.

Portugal has one of the most accessible residence permit schemes in Europe

We are proud to have a 100 percent approval rate on all applications submitted – a testament to our comprehensive local knowledge. Our team will be your guide through everything from investment consultancy, legal support, tax optimisation and representation, to liaising with the Portuguese authorities regarding your residency visa, to offering advice regarding all aspects of your personal and corporate presence in Portugal. Whether you would like to open a bank account or are in need of property management services, you can trust our team to deliver with integrity and professionalism.

Our real estate investment service is itself comprehensive. We are a client-oriented real estate agency providing our investors with the most profitable and adequate investment opportunities that can range from luxury villas – gems of contemporary architecture with private pools in tourist hot spots – to modern apartments in the heart of Lisbon. All of your golden visa consultancy needs will be met, from legal requirements, banking services, tax optimisation and property management. The wide scope of our integrated services is what makes our business different – and special.

Global living in the new normal

At PTGoldenVisa, we have done everything in our power to tailor our services to the restrictions of the pandemic – and have been very pleased with the results. Usually operating in offices in both Portugal and Dubai, we have adapted the company structure to allow residency permit applications to be made remotely. We understand how important investment selection is, which is why providing as much information as possible to ensure that our clients feel safe and comfortable in their decision is our priority.

Clients have been able to evaluate potential property investments through detailed videos, 3D presentations, virtual tours, location and financial analysis, and live video streams from the property. For those applying through investment funds, we have co-ordinated liaison with fund managers. We also provide online legal services and can open bank accounts remotely, among many other means of assistance. In 2020, we assisted more than 150 clients successfully while fully remote. The pandemic has driven interest in holiday homes for investors’ use, particularly in the privacy and security that a villa can offer. PTGoldenVisa is assisting with an increase in off-plan luxury villas in the proximity of big cities. Low supply and high demand mean that these projects offer capital appreciation of 15 percent a year.

The COVID-19 pandemic has, above all, brought instability and uncertainty to both the economy and our social lives. More than ever, people are reconsidering the future, and looking at golden visas as a road to safety and security. Our golden visa programme is more popular than ever. Though the tourism industry worldwide has been affected by travel restrictions, the capital appreciation on real estate in Portugal’s cities – 14 percent in the first quarter of 2021 – means that the golden visa programme has remained a safe investment. Great returns, a fantastic culture and future security awaits. Portugal looks forward to welcoming you.

During the pandemic, the financial market has become increasingly volatile, and this has consequently escalated so that more people are now becoming involved with financial trading. Georgios Argytakis, executive director of Just2Trade, spoke to World Finance about how his international investment company has managed during the pandemic. He also gives advice on how to choose a broker right for you, and predicts what the future steps will be for Just2Trade’s industry.

What is the financial situation that Just2Trade is currently in?

Just2Trade currently has a market leading position in attracting customers from more than 20 countries in Europe and Asia. Our clients have invested more than $400m, and collectively they have more than $50bn in annual trading activity in equity, bonds and derivatives. These figures by themselves speak volumes regarding our current situation, and clearly display our continuing success, despite the pandemic. Just2Trade has continued to comply with strict EU laws regarding protection of client assets and best execution client orders, and we continue to be regulated by supervisory authorities of the European Union. Just2Trade is also a member of the Investor Compensation Fund.

What innovations do you have planned for 2021?

Due to COVID-19, the market has become more volatile, and therefore an increasingly large number of people have become involved with financial trading. As a result of this increase, the equities, FX, CFD, cryptocurrency and other markets have experienced a significant uptick in trading activity. In view of the constantly evolving environment, Just2Trade will focus on developing its technological infrastructure and enriching the product range offered to its clients even further.

The recent advances made in technology has allowed investors to trade like experts, and this has therefore offered them the opportunity to access a wider range of financial markets and instruments at even lower costs. There is consequently a strong interest shown from investors for technical investment platforms, and that is where we come in. As a result of the increased interest, Just2Trade is developing new intelligent platforms that use a large amount of data to run predictive models, which come with stock ratings based on technical and fundamental analysis.

More people are seeking out ways of securing their future, so that they are safe regardless of what events occur

Through further development of our current technological infrastructure, and trading platforms, we aim to further reduce our cost structure, and offer even more competitive prices to our clients, so we can support them at an affordable rate. Most of our competitors are hindered by outdated systems with significant gaps in their technology, which only adds to their complexity, increases their cost, and slows down operational stability. Unlike these competitors, Just2Trade has not fallen into this trap. This is because we continue to invest in new technologies and trading platforms, and most importantly, we invest in our staff, all of whom are highly skilled and qualified people.

How would you advise someone who is going through the process of choosing a broker?

When going through the process of choosing a broker to work with, there are a few questions that we would advise a prospective investor to ask. These questions would start with asking if the broker in question has a proven track record and a solid market reputation, so you can ensure their reliability and previous success. It is also important for the client to ask if the broker offers the products and services that the client wants, so they can ensure they will get the service they need.

Other questions that we would recommend asking would be whether or not the broker is licensed and regulated, and if yes, are they regulated by reputable financial authorities? Is the broker a member of any kind of investor’s compensation scheme that protects investors in case of broker default?

Lastly, it is important for the client to find out if the broker segregates client assets from its own assets, to ensure that the client money is not at risk in case of default of the broker. If an investor has the answers to these questions, then they will be able to decide which broker is the right one for them and which will provide them with the best service.

Has the pandemic changed the way you do business with clients?

The pandemic has not significantly changed the way we do business with our clients. Our staff has continued to provide personal attention to each and every one of our clients, as they did prior to the pandemic. They are always on hand and ready to give them the very best level of support. The quality of our service remains one of the highest in the industry, and our client-centric approach, and core values of continually delivering our high levels of service remain unchanged.

How has Just2Trade been affected economically by COVID-19?

As mentioned previously, the pandemic has substantially increased market volatility, prompting a significant number of people to get involved with trading in the international financial markets. This increased market volatility has affected nearly all asset classes, which has consequently increased their risk to return ratio, and thus has made them more attractive. Overall, we think that the impact of the COVID-19 pandemic has been positive to the brokerage industry. However, competition still remains high, and the sole way to succeed is the same as always; to offer the highest quality service at the best price.

Why should someone open an investment account with you?

People should open an investment account with Just2Trade because we satisfy even the most demanding of investors, and are keen to support our clients in any way we can. Our company has an unblemished track record, as well as a proven history of doing business in the brokerage market. On top of this, we continue to offer new products and service lines to clients at the most competitive rates out there.

Just2Trade is established within the EU, and is therefore governed by some of the strictest laws in the world with regard to protection of client assets, as well as the best execution of client orders. Just2Trade is also licensed and regulated by the European Securities and Markets Authority (ESMA) and the Cyprus Securities and Exchange Commission (CySEC).

In addition, the company is a member of the Investors Compensation Fund, which compensates investors in the event of default of a member broker, offering our clients the safety and security they deserve. We also hold our clients’ assets separately from our own, and as a result of this safekeeping, client money and securities are never put at risk by any actions that the company takes.

How do you see the pandemic impacting the international investment industry?

We believe that the pandemic and the resulting restrictions in people’s movement will urge more people to look for investment opportunities through online brokers. We also think that as a result of the unprecedented times we have had, more people are seeking out ways of securing their future, so that they are safe regardless of what events occur. In addition, the combination of both the increased market volatility in the majority of asset classes, and the higher expected returns, are strong incentives to encourage people who have not previously done so to start trading.

“Yesterday I was clever, so I wanted to change the world,” the Persian poet Rumi wrote. “Today I am wise, so I am changing myself.”

The banking industry would be wise to change, too, and quickly.

In April, 43 global banks, including Bank of the West’s parent company BNP Paribas, joined the industry-led and UN-convened Net-Zero Banking Alliance (NZBA), committing their investment and lending portfolios to reach net-zero emissions by 2050. The NZBA is important to help meet the Paris Agreement’s objectives by mobilising the entire financial system to address the threat of climate change. Yet, not all of the major US banks, some of whom are the largest funders of fossil fuels, joined this global effort to reduce and track emissions. We can’t solve the climate crisis without banks.

Our low-carbon future depends in part on banks not making the climate crisis worse by underwriting carbon-intensive industries

Even if greenhouse gas emissions stopped today, lingering carbon dioxide in the atmosphere would keep global temperatures from cooling anytime soon, according to the National Academy of Sciences and the Royal Society. This raises the urgency for banks – including those making pledges to protect the planet – to take more substantive steps regarding their portfolios. Research from the non-profit CDP finds that emissions attributed to banks’ investing and lending activities are 700 times larger than emissions from banks themselves.

Bank of the West took action years ago to ensure that what it does and doesn’t finance are in line with supporting the planet’s health. We don’t have all the answers, and we know there is more work ahead, but the lessons we’ve learned along the way may be helpful for others in our industry to effect change.

We must close the climate financing gap

Financing targeting the climate crisis grew in 2018 to $546bn, with the private sector providing the majority at $323bn, according to the Climate Policy Initiative (CPI). However, the UN says up to $3.8trn is needed annually until 2050 to prevent an irreversible rise in global warming. We need to close this financing gap and soon. Private-sector banks have an important role. In fact, banks doubled their share of climate finance between 2013 and 2018 (see table).

Motivations matter

In 2017, Bank of the West implemented policies that restrict or prohibit financing of certain environmentally harmful activities, such as fracking and Arctic drilling. And in 2018, the bank committed $1bn over five years to finance a renewable energy transition. Our policies are publicly available, and we are well on our way to meeting our financing goal.

As part of BNP Paribas, we were motivated to act because we believe the private sector has a global responsibility to proactively address the climate crisis. We were driven by purpose.

Global finance can be a game changer

A planetary crisis affects us all. With that in mind, Bank of the West has used its global reach for the betterment of our customers and the planet.

For example, we’re providing working capital to the US subsidiaries of major European energy companies, supporting the growth of renewable energy generation across North America. This is part of our three-pronged strategy focusing on the development of renewables, cleantech and sustainable finance across industries.

We’re also using our balance sheet to encourage corporate borrowers to meet more ambitious social and environmental goals. Building on the industry-leading expertise of BNP Paribas, Bank of the West launched its sustainability linked loans offer in April.

What isn’t financed makes a difference

What banks stand for and what they finance are critical. So is what they decide not to finance. Our low-carbon future depends in part on banks not making the climate crisis worse by underwriting carbon-intensive industries. We know restricting financing based on principles is not easy because we have been on this path for a while. And we stand with the 43 global members of the UN’s NZBA because we firmly believe it’s necessary for the planet.

I’m humbled by the immensity of the task before us to stop the climate crisis. I also believe our global industry, collectively, can make a significant difference.

As the biggest banking group in Central America, with operations throughout the region, it is unsurprising that BAC Credomatic would lead the way in digital penetration for banking in the area. With a key customer base of individuals and SMEs, however, COVID-19 hit the region with no less force than anywhere else, and while technology and innovation remained vital, so too was retaining the personal feel people also needed in the midst of a pandemic.

Say ‘digital banking’ and you will likely think of mobile and online banking platforms. In fact, digital banking requires a complete transformation of all activities, programmes and roles, the automatisation of all banking processes, and the digitalisation of middleware, in order to get the different tools and systems to exchange information. In the banking industry, the transformation from traditional towards digital banking has been shaped by new technologies such as the cloud, big data and artificial intelligence.

These new technologies have forced the industry to improve customer experience in order to retain clients while staying ahead of the game. This means creating high-value digital services, ensuring their viability, and optimising their efficiency and profitability. The risk of not doing so is to alienate a client base in a region that still has problems with financial inclusion and a high proportion of unbanked populations.

At BAC Credomatic, therefore, the focus has been on listening to customers, monitoring customer interaction through digital platforms, and pivoting and adjusting the customer experience in order to make it simpler and more accessible. These efforts to streamline internal processes and improve their platforms have allowed the company to make great leaps in its digital adoption indicators.

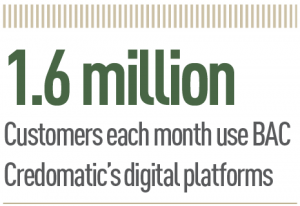

BAC Credomatic’s digital customer penetration grew by almost 10 percent between 2019 and 2020 (from 33 percent to 42 percent). Over 1.6 million customers access its services via digital platforms every month, and four out of five do so through its mobile platform. Of course, the unavailability of banking in-branch accelerated this adoption more than it would have if the pandemic had not struck, but BAC Credomatic always intended to develop and innovate in this way.

Customer-driven innovation

Constant innovation is a strategic priority for all forward-thinking banks, and in fact the journey towards a more digital and customer-centric organisation began in 2017. The aim is to offer solutions that although complex from a behind-the-scenes perspective, actually make the customer experience seamless and straightforward, driven by a strategy focused on what customers in the region actually need.

Its digital banking platforms are not simply a by-product of that digital transformation.

The bank also made great progress with its customer service channels, which ensured customer interactions were smooth and agile

Robust online and mobile banking platforms allow customers to carry out virtually any type of transaction, but the bank has also taken the digital transformation to its physical assets. This led to branches being redesigned to emphasise relational banking and create well-thought-out spaces for self-servicing, meaning customers still have a physical place to bank should they wish, but are given more autonomy and convenience while doing so. The bank also made great progress with its customer service channels, which ensured customer interactions were smooth and agile.