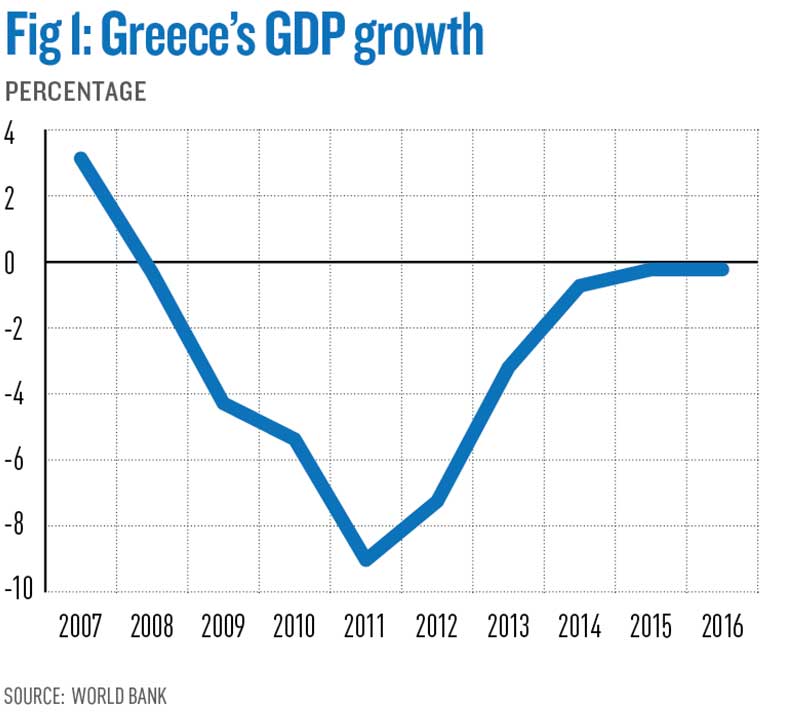

As with other oil-producing nations, Nigeria’s economy has been a mixed bag. In 2016, it experienced its first recession in a quarter of a century. It was an undeniably difficult year for the country as its finances bore the brunt of low oil prices. The situation was further exacerbated by a simultaneous reduction in output, caused by a series of militant attacks on crude pipelines in the Niger Delta.

In line with its socially conscious approach, Zenith Bank encourages gender equality and ensures that equal opportunities are offered to all

Last year, however, told a different story. After 15 months of recession, Nigeria’s economy finally rebounded in the second quarter of 2017, albeit at a GDP growth rate of just 0.6 percent. According to Nigeria’s National Bureau of Statistics, the economy achieved 0.83 percent growth overall for the year. Despite being slight, the figures are a positive sign of progress. In particular, they demonstrate the boost given to the oil sector thanks to a fall in the number of attacks on pipelines, which enabled production to increase by a third. Meanwhile, global oil prices also increased, helping to further bolster the economy.

Nigeria’s non-oil sector also played a significant role in the positive results of 2017. The adoption of a flexible exchange-rate policy, which aligned the naira with the black market rate, engineered a much-needed reduction in the shortage of dollars affecting importers. Accumulatively, a brighter economic and political outlook has been enticing investors back to Nigeria and the country’s stock market has rallied.

Against this bright backdrop, the financial sector continues to make significant moves, including the introduction of new technologies, which in turn have drastically improved the efficiency of financial transactions for customers. Various banks are also making a big push in terms of sustainability, creating better conditions for local communities and the environment alike. As an industry leader in Nigeria, Zenith Bank is a role model for both.

In light of the impact that the bank is having, both on the Nigerian financial sector and on local communities through an extensive set of corporate social responsibility (CSR) initiatives, World Finance spoke with the chairman of Zenith Bank, Jim Ovia, to find out more about the institution’s successes.

Laying the foundations for success

To understand how Zenith Bank is succeeding, it is important to go back to the very start. Established in May 1990, Zenith Bank began operating as a commercial bank in July of the same year. After 14 years of rapid growth and a highly successful initial public offering, the bank was listed on the Nigerian Stock Exchange in June 2004. The bank is also listed on the London Stock Exchange (LSE) and the Irish Stock Exchange (IRS). The bank’s listing of the second tranche of the $500m Global Medium Term Note programme broke ground with an overwhelming oversubscription of more than 300 percent. With its headquarters in the commercial capital of Nigeria, Zenith Bank now has more than 500 branches and business offices across the entire country – including, importantly, one in every state capital and major town in Nigeria. In 2007, it became the first Nigerian bank to be granted a licence by the UK’s Financial Services Authority, while it also operates in Gambia, Ghana, Sierra Leone, South Africa and China.

1990

Zenith Bank was established

2004

Bank floated on the Nigerian Stock Exchange for the first time

2007

The bank became the first Nigerian institution to be granted a licence by the UK’s Financial Services Authority

2013

Zenith Bank floated on the London Stock Exchange for the first time

In 2013, continuing along this path of expansion, the bank listed $850m shares on the London Stock Exchange, marking another major step in its status as a globally positioned financial institution. Today, Zenith Bank is the largest bank in Nigeria by Tier 1 capital and boasts a shareholder base of over one million.

“When Zenith Bank was founded, the intention was to meet the needs of Nigerians by providing excellent banking services,” Ovia explained. Given this steadfast focus on meeting the evolving demands and requirements of customers, the bank has placed cutting-edge technology at the core of its strategy. Consequently, by adopting the very latest innovations in fintech, Zenith Bank is able to provide platforms that are easy and intuitive to use, while also ensuring that transactions are carried out seamlessly, both online and in real time.

“From the beginning, the objective of the bank was to become and remain the leading brand in Nigeria,” Ovia continued. “That is why we have always strived to carve a global presence – and we have achieved this by offering a distinctive range of financial services. Since 1990, we have committed ourselves to building the Zenith brand into a reputable international financial institution that is recognised for innovation, superior performance and the creation of premium value for all stakeholders.”

In order to uphold this reputation, Zenith Bank maintains a continual state of evolution, constantly developing its services and adapting to shifting environments and customer taste. Ovia continued: “Over the years, business conditions have continued to change each year, bringing with them new prospects and challenges. That said, our objectives continue to be the provision of excellent financial solutions to our growing customer base across the world – and to do so in a way that creates value for all stakeholders.”

Thriving through technology

In order to stay at the top – and, in turn, provide the very best in financial services for its broad customer base – Zenith Bank is always on the look-out for new solutions that can improve the level of convenience and efficiency offered to its clients. Given the changing nature of financial services these days, it comes as little surprise that Zenith Bank has recruited Africa’s finest tech talent to work on new tools and platforms for the benefit of its customers far and wide. This is to complement its status as the company with the highest number of chartered accountants by any Nigerian institution.

“Zenith Bank is a trailblazer in the adoption of cutting-edge technology to provide banking solutions, which is why we are the bank of choice for millions of Nigerians,” said Ovia. “Our IT infrastructure is second to none in Nigeria, which is due to the fact that we have been able to adapt to the changing needs of the banking public by constantly coming up with new solutions. Our customer service is one of our pivotal attributes, upon which our institution has continued to thrive and won numerous endorsements and recognition for.”

As with any organisation worth its salt, Zenith Bank is all too aware of the importance of keeping clients happy. “We place the utmost emphasis on customer service, as we recognise that our customers are the primary reason of our business,” Ovia explained. In order to provide such excellent service, Zenith Bank places a lot of focus and resources into the development of its employees. He continued: “Our people are the greatest asset of our institution. We hire, train and retain the most diligent and highly motivated individuals that imbibe the vision of our institution.” It is to this approach that Ovia attributes the bank’s development. “Zenith Bank has grown organically,” he said. “Even when others have taken the M&A route, we have grown bigger and more sustainably due to the careful attention we have paid to retaining the best talent that Nigeria has to offer.”

Crafting a sustainable future

Over the past decade, sustainability has certainly become the buzzword of the corporate world. Much of this is based on a growing public awareness, which sees individuals opt for purchases and services that are less harmful to the world around them. As is the case with other spheres, this shared social consciousness has certainly made its way into the financial sector and transformed the way banks function.

The bank is involved in various community projects, including those dedicated to education advocacy, youth and sport empowerment and environmental sustainability

Given its size and leading position, CSR has become a core driver for Zenith Bank. According to Ovia: “It is necessary that banks operate with awareness and confidence – that their products and services do not have negative social and economic impacts on the environments in which they operate. This is crucial for the financial industry because every project they fund and every business banks invest in can affect the environment and local communities. This is why banks always conduct their business activities responsibly, without compromising the wellbeing of future generations.”

He continued: “For instance, in performing the crucial function of financial intermediation in the economy, sustainable banking requires financial institutions to deliberately channel funds away from investments and activities that harm the environment or cause social disorder. Instead, they should be channelled into areas that are environmentally friendly and enhance social development.”

As is the case with any nation working hard on its continued development, sustainable banking is crucial to the Nigerian economy. As stated by the Brundtland Report from the United Nations World Commission on Environment and Development: “Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs.”

Ovia said: “A safe and sustainable energy pathway is likewise crucial to sustainable development – this is something we have not yet found, but the rates of increasing energy use have been declining, at least.”

This point regarding clean energy is crucial for a country in the midst of large-scale industrialisation and agricultural development. When also combined with rapid population expansion, the energy required is enormous. “A safe, environmentally sound, and economically viable energy pathway that will sustain human progress into the distant future is clearly imperative,” Ovia told World Finance. “This, however, will require new dimensions of political will and institutional cooperation.”

With regards to urban areas, Ovia explained that good city management requires the decentralisation of funds, other resources and the will of local authorities, which are best placed to appreciate and manage local needs. “I agree that the sustainable development of cities will depend on closer work with the majorities of urban poor, who are the true city builders – namely, tapping the skills, energies and resources of neighbourhood groups and those in more informal sectors of work. Much can be achieved by the site and service schemes that provide households with basic services and help them to get on with building sounder houses.”

The benefits of sustainability

When asked how financial institutions can become more sustainable, Ovia replied that it involves carrying out banking operations and business activities with conscious consideration for the environmental and social impacts of those activities. “Sustainable banking integrates environmental and social criteria into traditional banking, and sets environmental and social benefits as a key objective,” said Ovia. “Financial institutions can become more sustainable by improving their activities to ensure that they create a very healthy environment, and they do the best they can in closing the social gap.”

There has been a major shift in sustainability when it comes to banking. This is in large part due to the kudos that comes with such actions. As indicated by survey findings, there are numerous reputational benefits that come with fulfilling regulatory requirements, which unsurprisingly act as the most common trigger for the adoption of sustainable banking practices. “Operational benefits – for example, increasing efficiencies and improving transparency – are the third most common trigger for banks adopting sustainable banking,” said Ovia. “The next most common trigger is the need for more employee engagement in terms of attracting and retaining talent. These top four triggers are in line with global trends, as demonstrated time and time again in recent years. But, as mentioned, the most common triggers for sustainable banking efforts remain the reputational benefits that come with meeting regulatory requirements.”

This shift is major news for Nigeria, to the extent that most banks in the country now compile annual sustainability reports that are submitted to the appropriate regulators. Zenith Bank has taken a lead in this direction, being the first company in Nigeria – and the first financial institution in the whole of Africa – to have adopted the GRI Standards in sustainability reporting.

“Zenith Bank promotes sustainability in terms of services and operations by making sure that sustainable business practices with reference to the environmental and social criteria of GRI Standards are embraced and executed. The bank adopted the green business option, which is committed to carrying out periodic reviews of our processes to identify areas of potential adverse environmental effects and mitigate them as efficiently as possible,” Ovia told World Finance.

He continued: “Zenith Bank is also conscious of the rising global concerns about environmental sustainability and has chosen to embrace ‘clean Earth’ principles. Our goal is to transform our banking operation into one that delivers low carbon emissions, energy efficiency, natural resource preservation, and protection of biodiversity and the Earth’s flora and fauna. We are fully dedicated to conducting our business activities in an environmentally friendly manner. The bank is mindful of the impact our business decisions could have on the career growth and overall wellbeing of our employees, and so these decisions are made with in-depth considerations.”

Zenith Bank also remains committed to adhering to all applicable labour laws and regulations in the different markets in which it operates. Consistent with international best practices, the bank establishes policies and guidelines covering grievance reporting and resolutions, disciplinary and reward procedures, paid maternity and paternity leave, employee training and performance management, and severance and separation benefits, among others.

Championing social initiatives

In line with its socially conscious approach, Zenith Bank strongly encourages gender equality and ensures that equal opportunities are offered to all personnel. “The bank strives to maintain a level playing field for all genders,” added Ovia. “As of December 31, 2016, we had a total of 5,970 staff in our employment, 2,859 of which are female and 3,111 male, representing 47.9 percent and 52.1 percent of our total employees respectively. There are 75 employees in the ranks of our top management group, which includes assistant general managers, deputy general managers and general managers. Of this number, 23 are female and 52 are male: the former represents a ratio of 31 percent.”

The bank is also involved in various community projects, including those dedicated to education advocacy, environmental sustainability, and youth and sport empowerment.

There is Zenith Bank’s multimillion-naira flagship Iga-Idunganran Lagos Island Community Healthcare Centre – a testament to its commitment to healthcare delivery in local communities. Not only did the bank fund the construction of the facility, but it also fully equipped it in order to meet the primary healthcare needs of Lagos Island residents. Along this vein, Zenith Bank donates equipment and facilities to hospitals across Nigeria, an example being its recent donation of incubators and other equipment for neonatal care to the University of Calabar Teaching Hospital in Cross River State in a bid to help reduce infant mortality.

Elsewhere, at institutions like the national hospital in Abuja, the bank has donated state-of-the-art ambulances, while it continues its work to help with the early detection of life-threatening diseases such as cancer and AIDS by providing free medical diagnosis kits to healthcare institutions. Other projects currently in the pipeline include a library project, which will see the bank fund more than 100 new libraries across the country, in addition to renovating existing ones in various different states.

Projects such as these are essential for Nigeria’s continued economic development and the improved welfare and wellbeing of its population of 186 million people. When asked about the bank’s role as part of this progression, Ovia answered: “The bank understands that the private sector is often seen as a driver of the economy and, in playing its part, the bank’s projects (which are collectively labelled CSR initiatives) have helped to improve the health and welfare of socially-excluded populations, thereby positively impacting their social status, earning potential and the access they have to services and resources.”

The necessity of ethical governance

Banks nowadays can’t escape from the necessity of corporate governance in their day-to-day operations, as well as their overall vision and direction. As such, Zenith Bank places corporate governance at the core of everything it does. “I believe corporate governance is the way a company polices itself,” Ovia told World Finance. “Corporate governance is intended to increase the accountability of companies and to avoid massive disasters before they occur.”

5 million

Number of free spectacles Zenith Bank has donated to women and children in the Maryland and Yaba communities

500,000

Number of wheelchairs the bank has donated to women and children in the Maryland and Yaba communities

Ovia gave failed energy giant Enron as a prime example of the importance of solid corporate governance in the long-term, sustainable success of any organisation – whether large or small. Through regular meetings with internal members, including shareholders and debtholders, as well as suppliers, customers and community leaders, companies can effectively address the requests and needs of affected parties.

He continued: “Corporate governance is of paramount importance to a bank and is almost as important as its primary business plan. When executed effectively, it can prevent corporate scandals, fraud and the civil and criminal liability of the company. The bank’s image can also be enhanced in the public eye as a self-policing organisation that is responsible and worthy of holding shareholder and debtholder capital,” Ovia explained. “A bank without a system of corporate governance is often regarded as a body without a soul or conscience. If this shared philosophy breaks down, then corners will be cut, products and services will be defective and management will grow complacent and corrupt. The end result can be catastrophic.”

To avoid such disastrous circumstances, Zenith Bank goes to great lengths to ensure it complies with a solid corporate governance model. “Shareholder recognition is key to maintaining the bank’s stock price,” Ovia explained. “More often than not, however, small shareholders with little impact on the stock price are brushed aside to make way for the interests of majority shareholders and the executive board. Good corporate governance seeks to make sure that all shareholders get a voice at annual general meetings and are allowed to participate.”

According to Ovia, stakeholder interests should also be recognised by corporate governance. In particular, he explained, Zenith Bank takes the time to address non-shareholder stakeholders, which helps the company establish a positive relationship with both local communities and the media. To this end, board responsibilities are clearly outlined to shareholders in order to ensure that all board members are on the same page and share a similar vision for the future of the bank.

“Ethical behaviour violations in favour of higher profits can cause massive civil and legal problems down the road,” he added. “Underpaying and abusing outsourced employees or skirting around lax environmental regulations can come back and bite the company hard if ignored.” To prevent this from happening, the bank established a code of conduct regarding ethical decisions for all members of the board. “This is crucial, because business transparency is the key to promoting shareholder trust,” said Ovia. “Financial records, earnings reports and forward guidance should all be clearly stated without exaggeration or ‘creative’ accounting.”

Zenith Bank’s corporate governance policies do not stop there, however, with new initiatives soon being rolled out. “The bank plans on reinforcing its corporate governance with a view to ensuring sustainable growth by launching proactive reforms to enhance transparency, as well as efficiency and manoeuvrability,” Ovia explained. “We will continue to introduce governance measures on an ongoing basis, as is appropriate to our aim of being a truly global company. Through such measures, we can maintain the trust of a wide range of stakeholders and continue to grow, while simultaneously responding to changes in the operating environment.”

Given the centrality of corporate governance to its operations, the bank now acts as a role model to others in the country, as well as the wider region. In recognition of its efforts, Zenith Bank was the first bank in Nigeria to win the award for Best Corporate Governance from World Finance magazine for three consecutive years (in 2014, 2015 and 2016). “This demonstrates that the bank is miles apart from its competition,” said Ovia.

In terms of its future plans, the bank will keep steady on its course of sustainability, community support, environmental awareness and solid corporate governance. “The bank plans on keeping a keen eye on the future and taking action to protect it,” Ovia noted. “A great way to do this is by focusing on our staff, the environment and achieving sustainable profits, which will help us achieve our medium to long-term goals.”